Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Each Thursday, Asia House Advisory’s COVID-19 monitoring service examines the impact of economic measures taken by individual governments across Asia and the Middle East. This week, we look at India.

India has recorded 276,583 cases and 7,745 deaths from COVID-19. Despite implementing one of the world’s most stringent lockdowns, India now ranks fifth globally in number of cases. How has this impacted the national economy, and what could recovery look like?

On 24 March, the Indian government ordered all non-essential businesses to close and implemented a complete nationwide lockdown for six weeks. On 4 May, the government eased restrictions, dividing 700 areas in the country into green, orange, and red zones based on the number of cases recorded. Red and orange demarcated zones maintained strict lockdown measures, with little economic activity allowed to resume. Despite such measures, cases have surged, and the risk of further outbreak remains very high as the country further eases restrictions this week.

The government has introduced economic stimulus measures to cushion the damage: Prime Minister Narendra Modi in May announced a US$270 billion economic support package and the Reserve Bank of India has cut its headline interest rate and tabled packages of other monetary stimulus measures.

Despite this, national GDP has contracted as much as 13.5 per cent since the implementation of lockdown

India’s GDP in 2020 could contract anywhere between five and 6.8 per cent. By sector, COVID-19 and the resulting national restrictions have resulted in huge contractions across industries and states. The pandemic has increased market concern on weakening demand and supply chain disruption. Slow private sector capital expenditure, challenges to credit growth, and non-performing loan issues have already challenged the economy. Further supply chain disruption due to the pandemic and weakening demand have weighed on economic growth. In the near term, uncertainty over any recovery is likely to remain high as the impact and duration of the lockdown remains unclear.

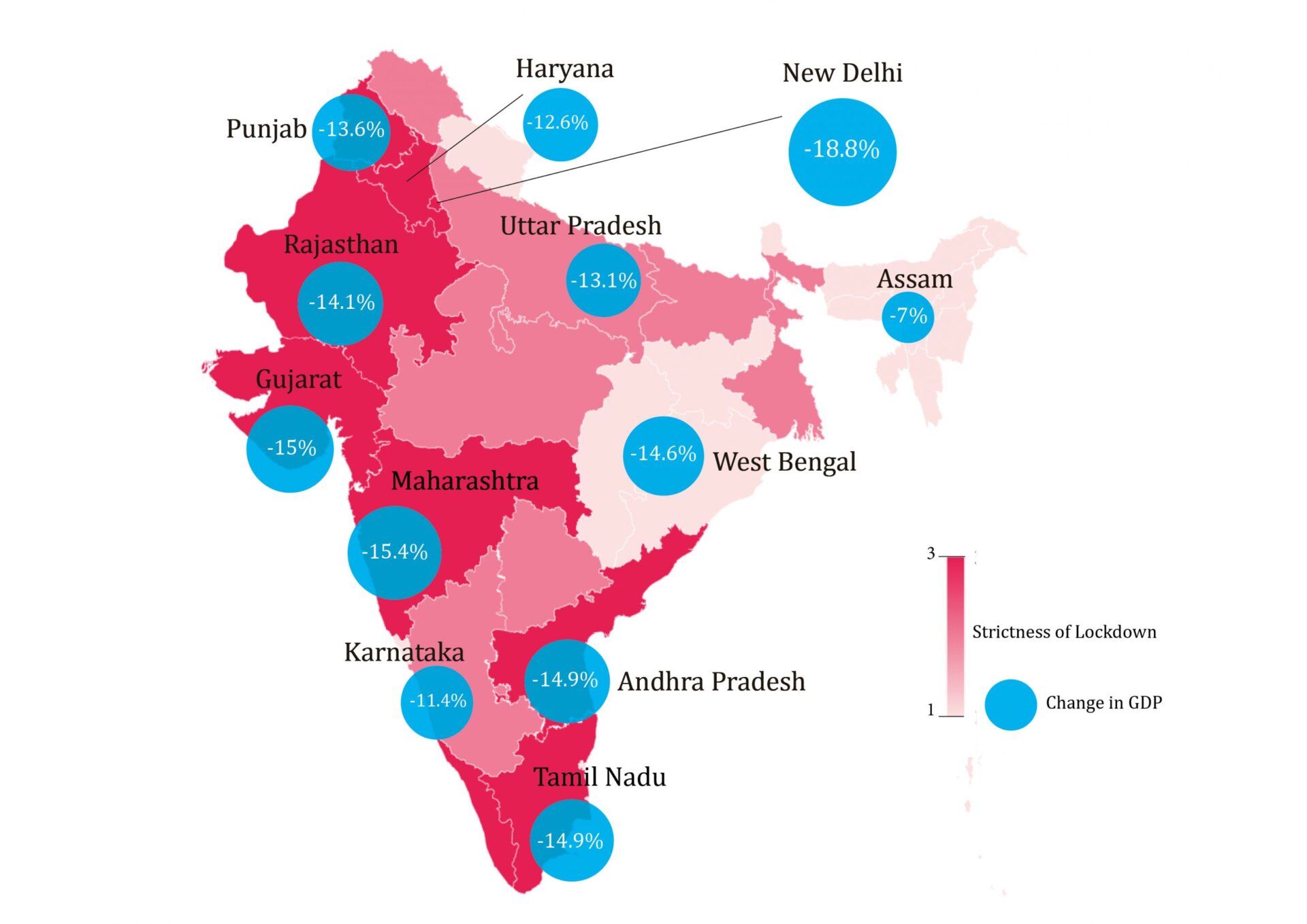

Key state by state: shading per state indicates the strictness of the lockdown measures within the state during India’s lockdown last month, calculated as a proportion of zones in each state which were designated as red, orange, or green by the government.

Graphic explainer

Though much of the country has opened up over the last week and resumed economic activity, between March and May 2020, states with higher proportions of red and orange zones saw lower levels of economic activity, whereas states with more green zones – which signified low numbers of COVID-19 infections – were allowed to resume more economic activity earlier than other states.

The numbers in the blue circles signify drop in state GDP during the lockdown seen in each state. Altogether, there has been a dip of close to 13.5 per cent in national GDP attributed to the impacts of COVID-19.

States with high concentrations of manufacturing and services activity – such as Maharashtra, Delhi, Tamil Nadu, and Gujarat – have seen both stricter and more prolonged lockdowns and a larger loss in state GDP. The combined loss from orange and red zones during the second phase of the lockdown represents close to 90 per cent of the total loss in economic activity.

States with ‘strict lockdowns’ – including Gujarat, Maharashtra, and Delhi, saw huge reductions in state GDP. These are also some of the states with the highest number of COVID-19 cases.

The services sector collapsed in April, falling from a Purchasing Managers’ Index (PMI) of 49.3 in March to 5.4 in April, and recovering only slightly to 12.6 in May – still marking a significant contraction. Manufacturing has been equally badly hit. These sectors – heavily concentrated in states including Maharashtra, Gujarat, Tamil Nadu, and the Delhi-NCR area – have seen massive reverse migration since the implementation of the lockdown. As much as 60 per cent of the labour force have left such manufacturing hubs to return to far-flung villages and are unlikely to return in the near term. So, despite the allowed resumption of most economic activity, there is an acute shortage of workers. With factories operating at below-normal capacity, the cost of production has risen and profits have fallen.

Reserve Bank of India Governor Shaktikanta Das last week suggested that the impact of COVID-19 on the domestic economy will be more severe than anticipated, with high-frequency indicators over the last three months suggesting a collapse in demand. Major parts of the economy are and will continue to operate below capacity. The stimulus packages announced will struggle to encourage growth in the short term, given its lack of planned government spending. Any benefits will only be seen in the longer term. Indian markets have fallen sharply this year as a result, down over 30 per cent in US dollar terms, and broadly outpacing declines in both global and emerging markets. Foreign investors have pulled US$16 billion from India.

These issues are compounded by longer-term weakness in the country’s financial system. The last few decades have seen a series of issues in the financial sector including bad lending decisions and a credit crunch. The stress in the financial sector, which was already contributing to India’s lowest expected GDP growth in over a decade this year, will threaten efforts to prop up the economy. Ratings agencies have cut India’s credit ratings, bringing it precariously close to junk status.

In the near to medium term, strong economic recovery will be tough. A lot will depend on the confidence of India’s huge migrant workforce to return to economic centres – the longer the labour force shortage, the slower the economic recovery.