Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

In a new research briefing, Phyllis Papadavid, Director of Research at Asia House, explores the economic trends in Asia that highlight the region’s particular vulnerability to rising oil prices.

FIND OUT MORE ABOUT ASIA HOUSE RESEARCH

Key messages

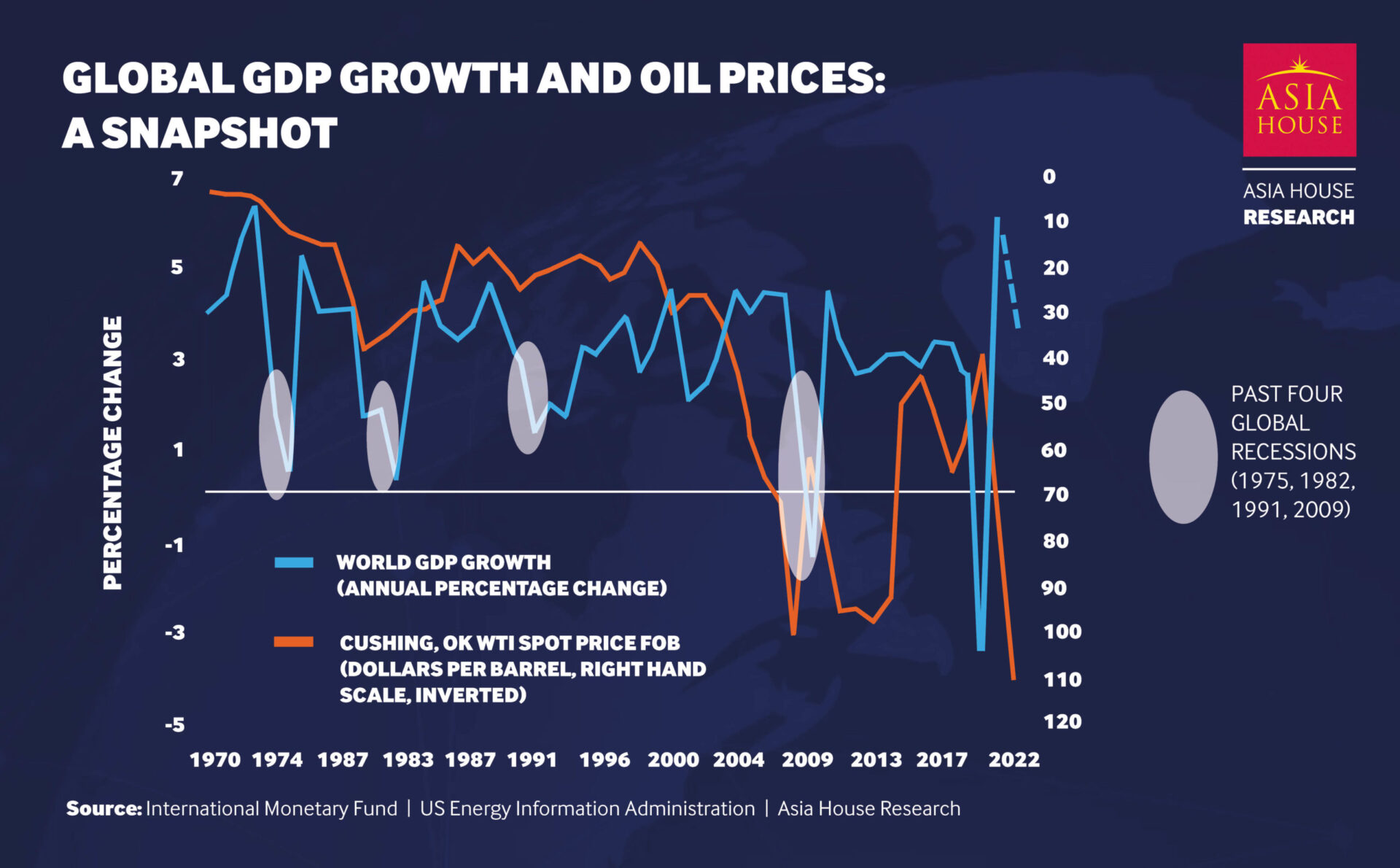

The increase in oil price, relative to last year, has been significant. As mentioned in the quarterly update of the Asia House economic readiness indices, this will impact Asia’s growth outlook. Gulf Cooperation Council economies, by contrast, are likely to see a boost to their growth outlooks. However, past oil price shocks have either led to – or coincided with – significantly weaker global growth (Figure 1).

Outright global recession[1] is not likely, and is not always easy to define. The global economy has rarely registered outright contractions. And yet, a significant global growth deceleration, or a ‘double dip’ could materialise. What’s more, the growing importance of emerging and developing economies in propagating and determining global downturns, given structural trade and financial linkages, will be decisive – particularly in Asia.

Figure 1. Global GDP growth and oil prices: A snapshot

Unexpected oil prices spikes are particularly impactful when they coincide with other shocks. And not all oil price shocks are the same. Oil price rises that coincide with geopolitical conflict have given rise to high risk aversion and lower economic outcomes. In 2008, during the global financial crisis, emerging economies fared better than their advanced economy counterparts. In 1990, rising gas prices amid the war in Kuwait had a significant impact.

Asia looks particularly vulnerable to this current oil price shock given existing vulnerabilities that are linked, in part, to the COVID-19 pandemic – such as economic scarring. Asia’s resource dependence, when it comes to oil, is large.

Given this, the region looks to be the most vulnerable to a ‘double-dip’ in its growth trajectory owing to the following three factors:

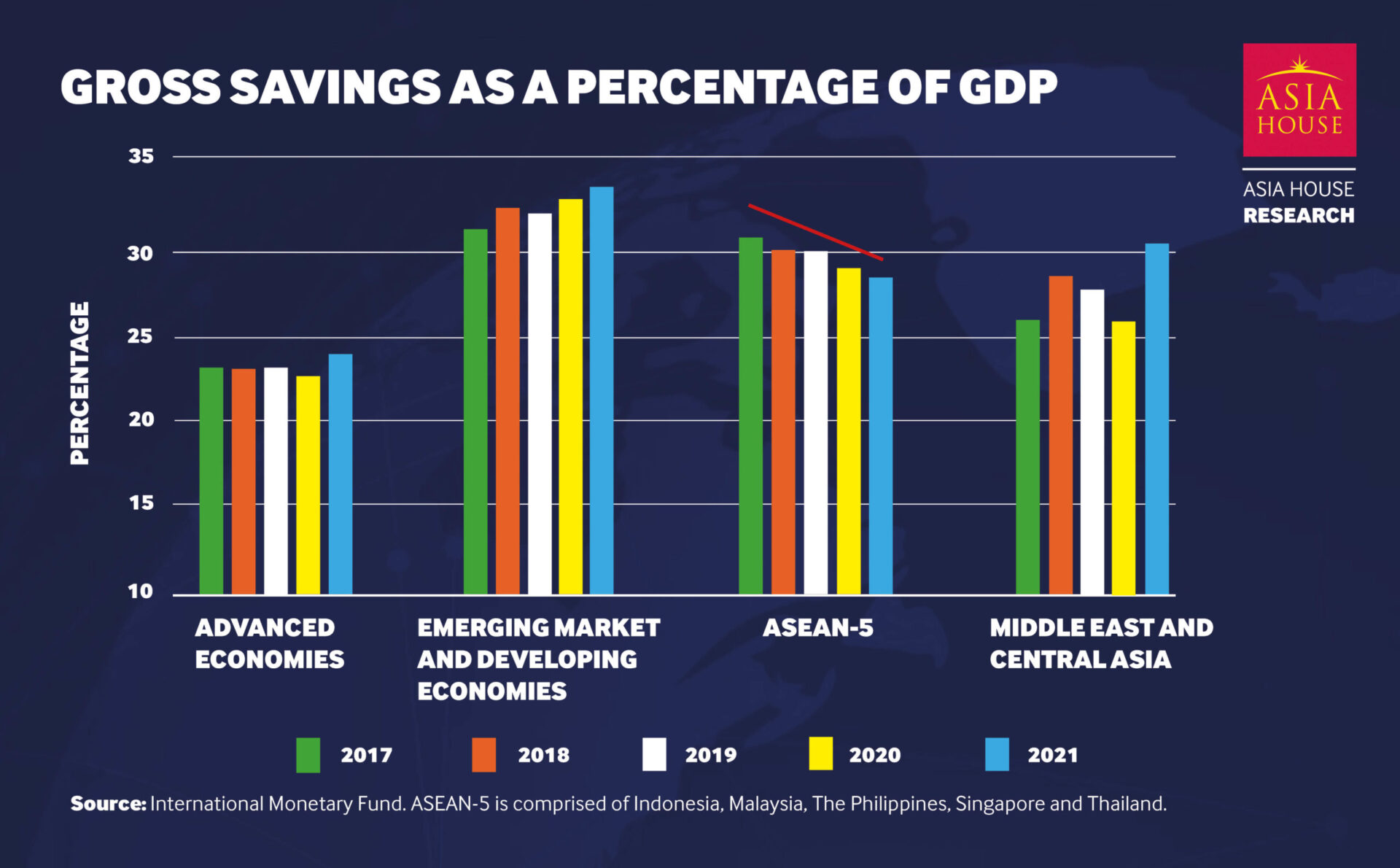

Asia’s household sector will see downside risks. Household budgets do not typically adapt well to large changes in gas prices and consumers (particularly in lower income cohorts and economies) consistently cut back expenditure when basic goods and utility prices increase. Gross savings[2] have been increasing in emerging and developing economies. However, while they remain high in ASEAN, there has been a notable downtrend since 2017. What’s more, the slow recovery in Asia’s consumption growth, coupled with its high oil consumption, makes the region particularly vulnerable to current oil price developments.

Figure 2. Gross Savings as a percent of GDP

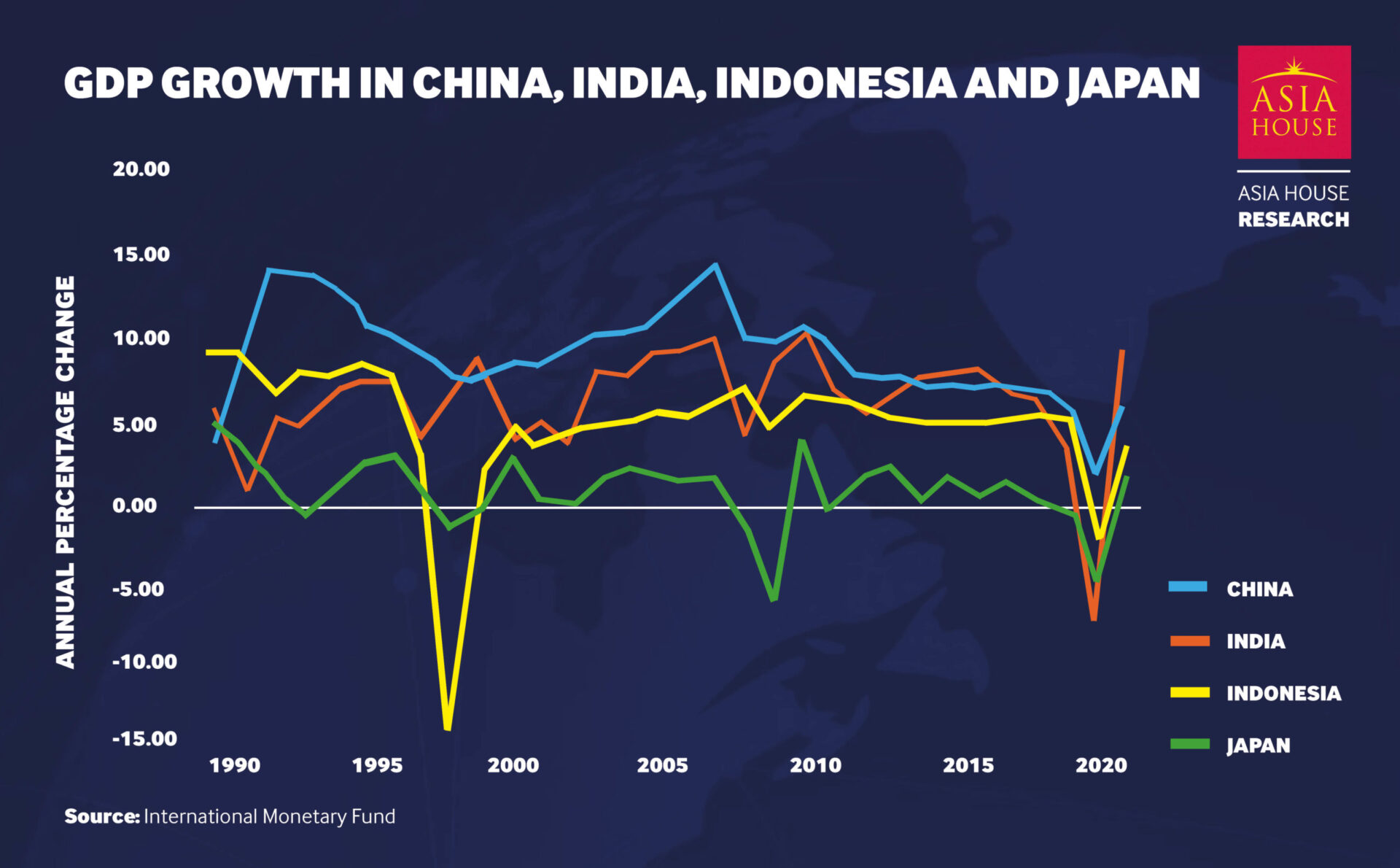

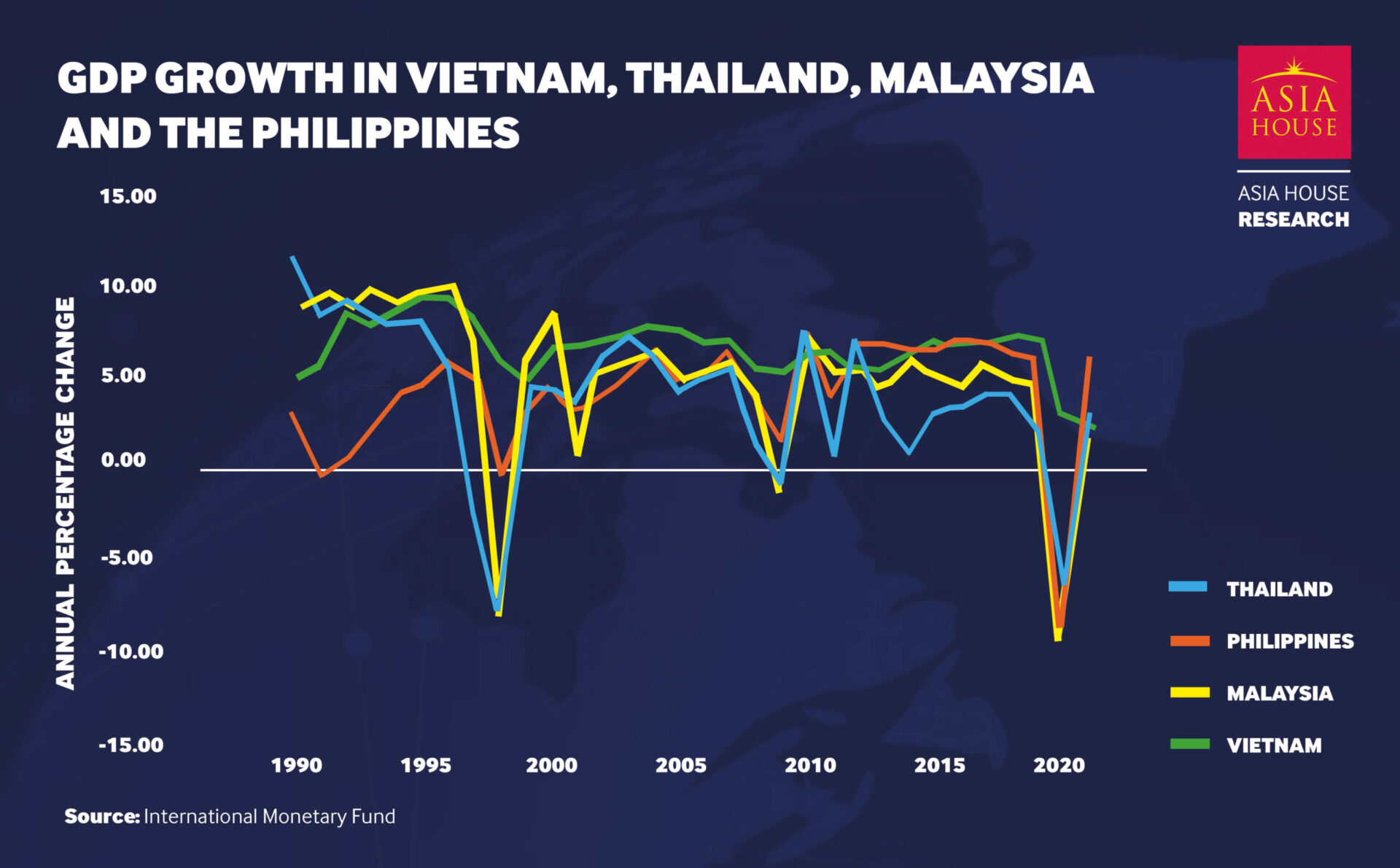

Asia’s fragile, uneven and early stage recovery is vulnerable to further shocks. Encouragingly, there have been signs of an interspersed economic rebound in Asia (Figures 3 and 4). However, the early stage of the recovery – both the unevenness in its composition and its structural imbalances – means that Asia’s constituent economies are more vulnerable to oil price (or any other shocks including unexpectedly faster than expected monetary tightening in the US). The particular risk linked to multiple shocks is that their pathways could become mutually reinforcing. For example, an increase in energy costs, food prices and a higher US dollar (the latter stemming from a higher US interest rate differential) could cause an inflationary spiral in a number of Asia’s economies that could prove difficult to contain.

Figure 3. GDP growth in China, India, Japan and Indonesia

Figure 4. GDP growth in Vietnam, Thailand, the Philippines and Malaysia

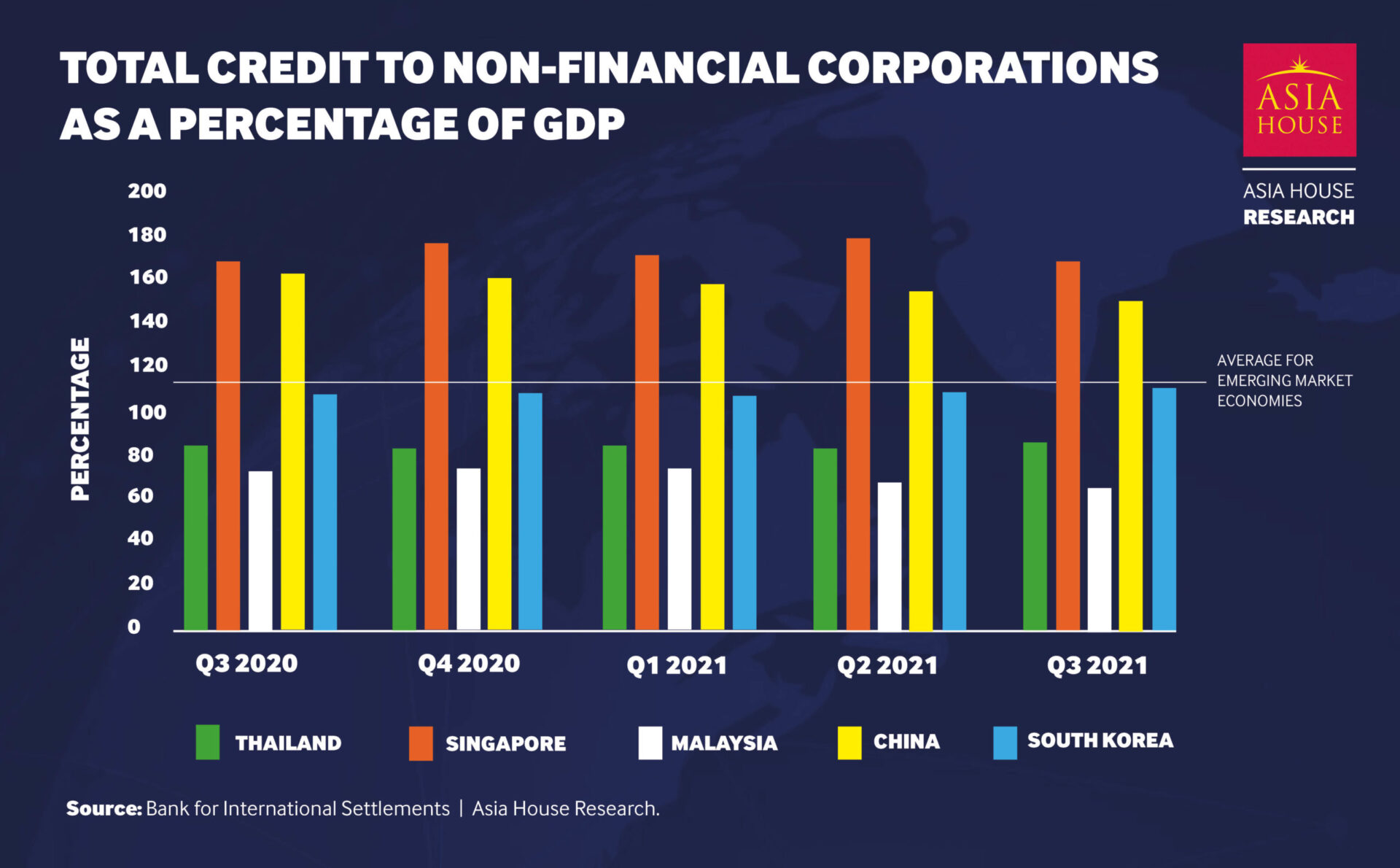

Asia’s credit markets could expose debt vulnerabilities. Corporate credit markets are starting to express a higher level of risk aversion amid tighter lending conditions. Rising corporate credit spreads are typically seen as an indicator of the end of an economic expansion, given that they denote, in part, higher borrowing costs for the corporate sector. As credit becomes increasingly scarce, and less affordable, it is likely that defaults are set to increase. Non-financial corporate debt increased following the 2008-09 financial crisis and is comparatively high in China and in other economies (Figure 5). This may be a source of deepening risk amid higher energy prices.

Figure 5. Total credit to non-financial corporations (as a per cent of GDP)

Economic scarring from COVID-19, geopolitical conflict and the continued rise in energy and commodity prices is likely to create persistent uncertainty in Asia this year. This, in turn, will hurt economic growth significantly (through both consumption and investment) as well as cross-border trade. Crucially, uncertainty about the outlook is also likely to limit policymakers’ ability to cushion against the most recent energy price shock.

Read more in the Asia House Annual Outlook

[1] Typically recessions refer to at least two consecutive quarters of decline in output, or a decline in global GDP per capital savings can be broadly defined as the difference between disposable income and consumption.

[2] Gross savings can be broadly defined as the difference between disposable income and consumption.