Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Asia House Advisory analyses the latest GDP data from Asia Pacific economies.

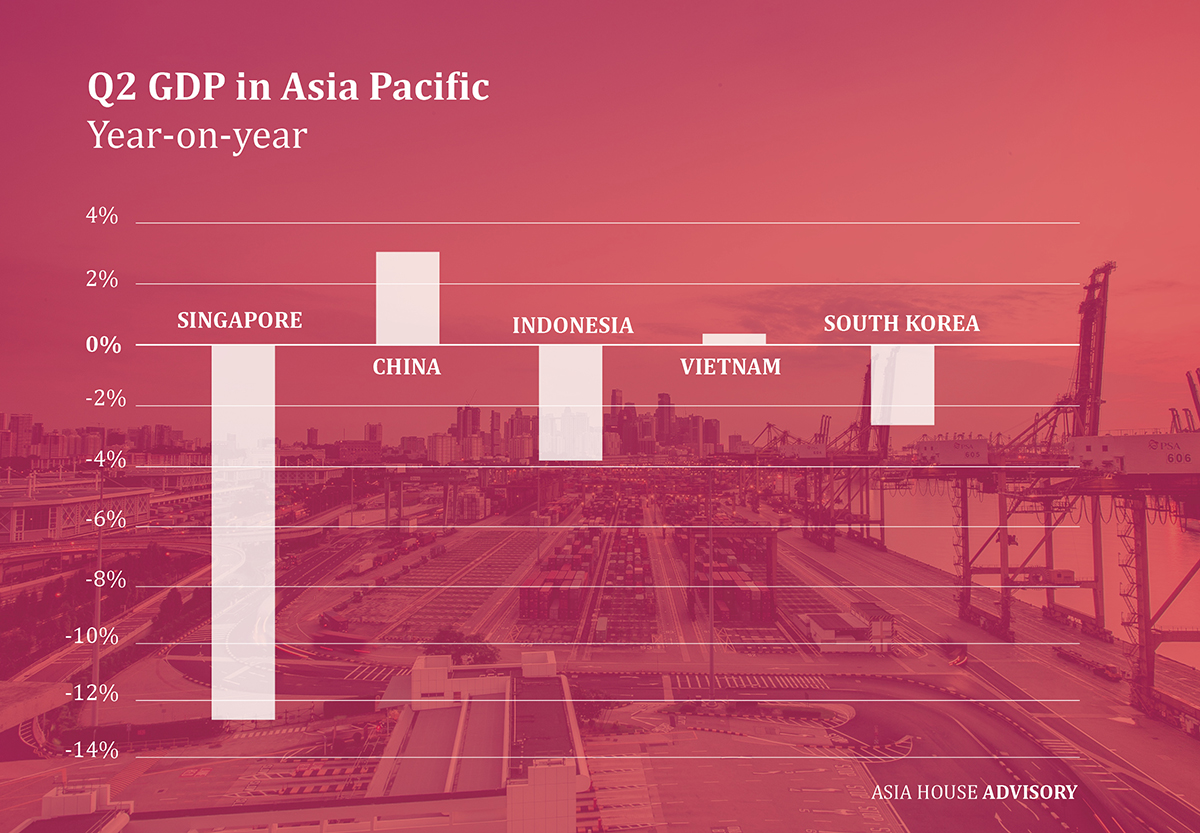

As Q2 2020 data is released by Asia Pacific (APAC) economies, the full extent of the economic impact of the COVID-19 pandemic is becoming apparent. Several economies saw a double-digit drop in quarterly GDP between Q1 and Q2, with many economies experiencing negative or static growth in Q2 compared to last year. However, China bucked the trend, reporting an upswing of 3.2 per cent year-on-year for Q2, a healthy increase from -6.8 per cent in Q1. Vietnam also just managed to maintain positive growth.

Several of the figures are astounding. Singapore entered a technical recession this year as it saw its economy shrink by 41.2 per cent between Q1 and Q2. Singapore will see a year-on-year Q2 GDP decrease of around 12 per cent. Meanwhile, analysts forecast an annualised contraction of more than 20 per cent in Q2 in Japan.

South Korea reported a 2.9 per cent year-on-year drop in Q2, the steepest decline since the Asian financial crisis in 1997. Indonesian Finance Minister Sri Mulyani Indrawati has predicted a 3.8 per cent year-on-year contraction this quarter and has significantly downgraded annual growth forecasts.

Many analysts are expecting to see a rebound in economic activity in the second half of 2020, as social distancing restrictions are eased. However, most Asian economies have had to maintain or ramp up containment measures in the last few weeks. Hong Kong has imposed its strictest social distancing measures yet; Australia has re-imposed a six-week lockdown in Melbourne; Thailand has extended its lockdown for a fourth time; Vietnam has seen its first local transmissions in more than 100 days and implemented strict measures in Danang; and Tokyo has seen record numbers of cases over the last weeks.

As a result, consumer spending has remained low. Singapore recorded a 52.1 per cent drop in retail sales in May; Japan is expecting a 6.9 per cent drop in consumer spending in Q2; and imports in China contracted 9.7 per cent in Q2. Though there are early signs of recovery in parts of the region, consumer demand remains muted.

Recovery will depend largely on how quickly consumer confidence can be restored, and whether there is a significant pick-up in private investment and consumer demand. If economic recovery is not private sector led, as expected, policymakers will not have as much room for economic and financial policy support going into next year, given the already heavy stimulus spending and prolonged economic contraction.

Issues that will continue to stifle recovery in APAC economies through the rest of the year include:

• Longer than expected or repeated lockdowns

• The reliance of many Asian economies on tourism or remittances

• The scale of the informal sector in many economies

• High debt levels

• Weak recovery of global demand

The last point is particularly complex. Asian economies rely on global demand, but also increasingly account for a larger share of global demand; APAC economies accounted for more than 70 per cent of global growth in 2019.

The region is an increasingly important place for economic demand and plays a vital role in the global economy. APAC will be central to global economic recovery from the crisis, not least because as the first region hit by the pandemic, it is also poised to see earlier recovery – in theory.

The resurgence of COVID-19 cases in many APAC economies is an early warning to the rest of the world, and could threaten the wider global economic recovery.

This analysis was prepared by Asia House Advisory, which provides bespoke consultancy services to help organisations understand new operating environments and develop engagement strategies to approach business-critical challenges. Find out more