Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Phyllis Papadavid, Director of Research at Asia House, looks at the UK’s recent export performance and highlights a need for the new UK government to pursue a more innovative trade policy in Asia.

Phyllis Papadavid, Director of Research at Asia House, looks at the UK’s recent export performance and highlights a need for the new UK government to pursue a more innovative trade policy in Asia.

The UK government’s post-Brexit trade strategy has been largely based on securing trade deals with markets outside of the European Union (EU). Much energy has been spent in pursuing and promoting trade deals in the Asia-Pacific, including high-profile agreements with Australia, Japan and New Zealand. However, UK exports to Asian markets continue to fall well short of pre-Brexit exports to the EU. Recent analysis estimates the UK’s losses due to Brexit as more than 178 times greater than its trade deal gains,1 suggesting that more needs to be done to boost UK exports.

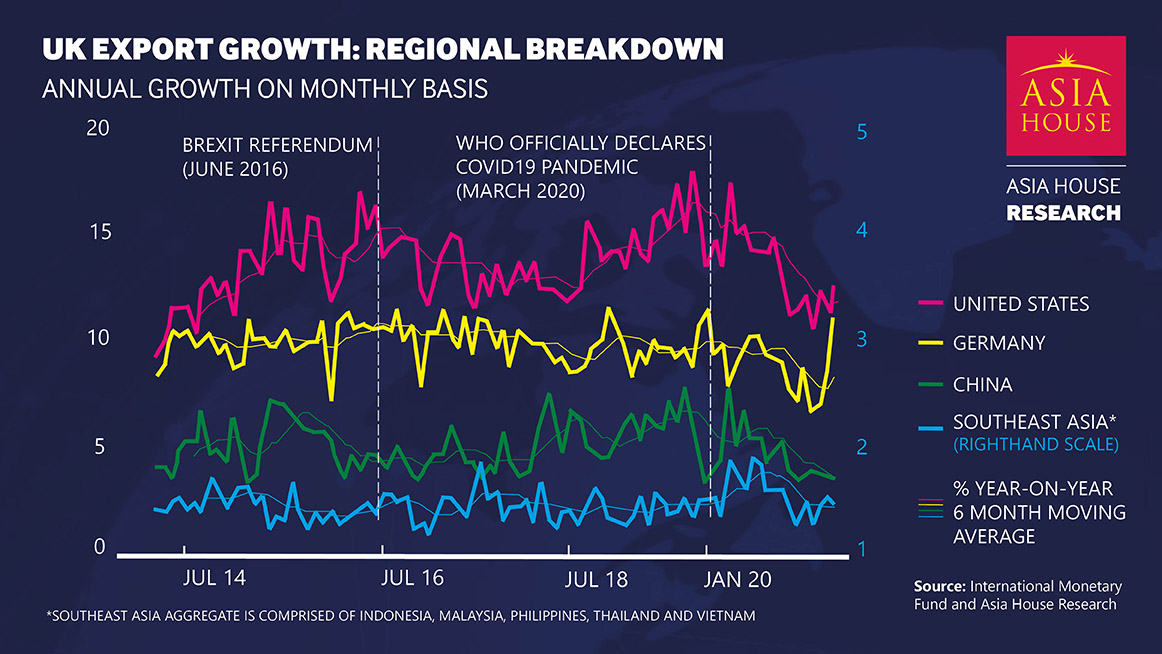

Since the June 2016 Brexit referendum, which led to the UK’s exit from the EU, UK export growth has largely stagnated, and in some cases decelerated, to both the EU and Asia. Asia-based export growth has not matched that of the EU, due in part to the COVID-19 crisis (Figure 1). Trade with Southeast Asia grew just 0.07 per cent, while trade with China fell 1.1 per cent between 2016 and 2021.

Asia does, however, hold considerable potential for the UK, but a paradigm shift in policy is required to realise this potential. Exports to Southeast Asia and China, for example, would need to register annual growth of approximately 15 and 20 per cent respectively each quarter for the next 18 months to broadly match UK exports to the Euro Area – highlighting how important the EU remains to the UK economy. Yet with the current political landscape limiting the prospects for more favourable UK-EU trade, and the UK particularly reliant on its trade and investment relationships, boosting trade with the Asian economies is critically important.

As the Conservative Party elects a new leader to serve as Prime Minister amid a challenging economic environment, this report outlines the importance of boosting UK exports to Asia and driving much-needed growth for an economy overshadowed by potential recession.

Figure 1: UK export growth by regional breakdown

The UK is highly integrated into the global trading system. Foreign developments account for around half of the variation in UK GDP and for over two thirds of the variation in measures of financial risk (Cesa-Bianchi et al., 2021). Total merchandise trade – the sum of imports and exports – is equivalent to approximately 55 per cent of UK GDP, more than the average across major economies.

Since the Brexit vote to leave the EU in June 20162 and the imposition of EU customs procedures in January 2022, the UK trade deficit has deteriorated, including to the EU.

The UK push for new trade deals has dominated the domestic policy landscape. The proposed trade deals have been a cornerstone of policy, although there is skepticism around the magnitude of the economic benefits – at least for some of the deals – beyond what would have been achieved under EU membership. The UK-Japan Comprehensive Economic Partnership Agreement (CEPA) is illustrative of this, with an estimated economic boost of 0.07 per cent. The UK-New Zealand deal, one of the UK’s greenest, is also estimated to have a negligible effect, relative to prior EU arrangements (Winters and Larbalestier, 2021).

The benefits of the raft of UK trade deals have yet to be seen and could take some time to materialise in the light of heightened global economic uncertainty. The UK comprehensive agreement with New Zealand, signed in February 2022, is forecast to increase trade between the two nations by 60 per cent by 20353 and includes the elimination of tariffs on all UK exports to New Zealand. The UK-Australia FTA contribution to trade is estimated at 53 per cent.4 Both FTAs aim to increase digital trade, and the digital facilitation of trade, that benefit creative industries, finance and telecommunications, and secure the free flow of data under key protections.

The UK’s second largest trading partner, following the EU, is the United States. In the four quarters to Q4 2021, total trade in goods and services was £215.2 billion5 accounting for 16.8 per cent of total UK trade. The prospects for a UK-US trade deal have been challenging, due in part to technical standards and regulations (UKTPO, 2019). Notably, the UK’s first state-level trade and economic development Memorandum of Understanding was signed with Indiana in May 2022.6 In order to reap the significance of US-UK trade, further efforts at bilateral trade liberalisation will be critical at a broader level.

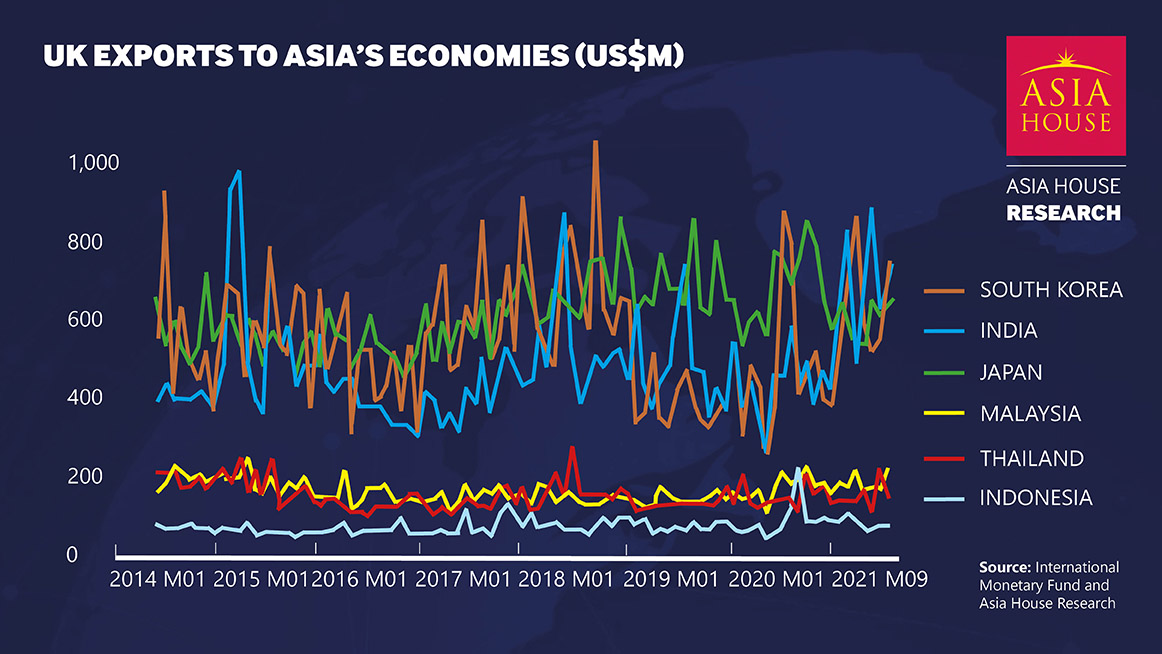

Asian markets could help make up the UK’s post-Brexit trade shortfall, but UK exports to Asia have not accelerated in a broad-based fashion, though India and South Korea have been relative bright spots (Figure 2). Our estimates suggest that further measures are needed to ensure trade growth with Asia.

Figure 2: UK exports to Asian economies

UK export growth to Asia needs to see acceleration to support the UK’s post-Brexit outlook. With a 55 per cent trade share of GDP, 7 the UK is a comparatively open economy, compared to, for example, the US’s 23 per cent share. And with an approximate 2.5 per cent of GDP current account deficit8 (and a decades-long external deficit position), bilateral trade – and particularly the promotion of exports – is essential for UK economic growth. Yet a lot of ground needs to be made up; bilateral trade with Southeast Asia and China will have to increase by 15 and 20 per cent annually, each quarter, for the next 18 months, in order to broadly match UK-Euro area trade (of approximately US$243 billion).

If the UK is to achieve anything near that rate of growth, a paradigm shift in trade policy with Asia is needed. There are, however, opportunities currently in play for the UK to grow its exports to Asia.

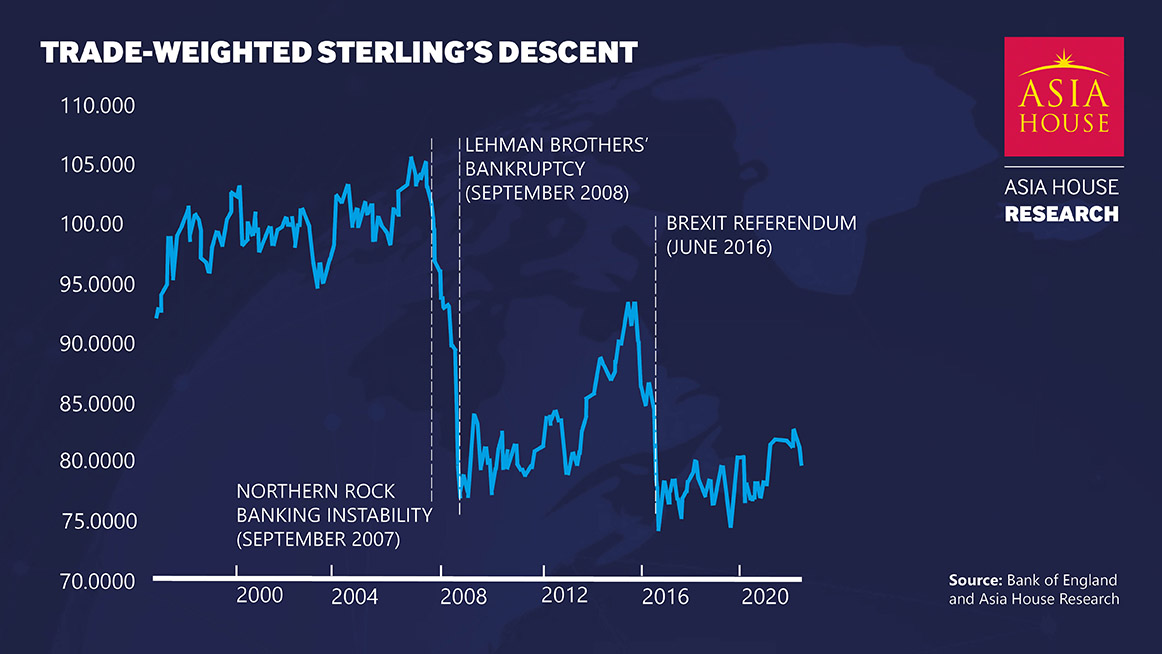

Sterling’s depreciation, coinciding with the policy push for new FTAs, offers an opportunity. The pound sterling exchange rate – a dual metric of both competitiveness and purchasing power when it comes to Britain’s trade position – has been stable at a weak level. In broader trade-weighted terms, it is likely to continue its descent (Figure 3). To maintain both internal balance and external balance, including through competitiveness effects, sterling is likely to find a lower footing; this could help boost the UK export share in Asia’s markets. This, however, might come at the cost of lower domestic purchasing power.

Figure 3. The UK pound sterling resumes its descent

The UK leveraging ASEAN Dialogue Partnership9 will support multilateralism and political traction. The ASEAN region is the world’s fifth largest economy and Asia’s third largest with a combined GDP of US$3 trillion.10 UK-ASEAN bilateral trade in goods and services amounted to over US$52 billion in 2019 and fell to US$46.1 billion in 2020. A multi-sector detailed strategy with ASEAN began with the negotiation of EU continuity agreements, but evolving trade relations with ASEAN beyond these could unlock trade growth.

During the first UK-ASEAN ministerial meeting in Cambodia, ministers agreed a Plan of Action for 2022 to 2026 – the first since the UK became an ASEAN Dialogue Partner. As part of the agreement, the UK will scale-up development and security links in Southeast Asia, opening a regional British International Investment office in Singapore later in 2022 to invest up to £500 million in the Indo-Pacific region (FCDO, 2022).

Accelerated FTAs in Southeast Asia: Indonesia and the UK are committed to a strategic partnership11 that is driven by global supply chain resilience, cooperation in trade and investment, creative economy, and digital technology – following the first UK-Indonesia Joint Economic Trade Committee (JETCO). Of particular significance going forward would be an FTA under the JETCO mechanism. Vietnam, an open and vibrant economy (Asia House, 2021a), is illustrative of this. A year after the UK-Vietnam Free Trade Agreement (UKVFTA) came into effect in May 2021, UK exports to Vietnam grew by over 20 per cent after the UKVFTA eliminated 99 per cent of all tariffs.12

The much-discussed UK-India trade deal is expected to improve market access for UK goods: with India’s plans to become a US$30 trillion economy by 2050, from the current US$3trillion,13 the UK will benefit from a growing market for its exports. A UK-India trade deal is expected by October 2022 which is estimated to boost bilateral trade by £28bn by 2035.14 Key trade catalysts would include the elimination of the 150 per cent tariff on UK alcohol exports to India and a new data adequacy agreement through the dedicated digital trade chapter (Parkin and Reed, 2022). And yet, the FTA is not a done deal: there remains skepticism in relation to elements of the proposed trade agreement and in relation to India’s business and regulatory environment.15

UK-GCC trade talks16 began in June 2022 and represent an important inflection point (Asia House, 2022) for UK trade. Formal negotiations started in August and are set to look at removing tariffs on renewable energy infrastructure such as UK-made wind turbine parts. Bolstering food security is a key theme in the FTA talks: discussions have flagged the possibility of the GCC reducing or removing tariffs on food and drinks imports from the UK, which currently range from five per cent to 25 per cent.17 Saudi Arabia is the UK’s largest trading partner in the GCC, accounting for one-third of its bilateral trade. Both sides are hopeful of securing a deal before the end of 2023.

A stabilisation in China-UK trade relations would be beneficial or UK exporters. China is one of the UK’s largest trading partners, accounting for £93.0 billion (7.3 per cent) of the UK’s total trade in 2021. The UK-China joint economic and trade committee (JETCO) were held annually until 2018, when bilateral relations deteriorated. While outgoing Prime Minister Boris Johnson has supported plans to re-open a second avenue of talks with Beijing, the prospects of improved trade relations appear increasingly distant amid a hardening rhetoric over UK trade with China in the Conservative leadership contest. The bilateral trade relations could be strained further by tensions over Taiwan, with China’s Ambassador to the UK, Zheng Zeguang, recently stating that a crossing of Chinese ‘red lines’ by the UK could bring ‘serious consequences for bilateral relations.’

CPTPP accession could boost digital reach. Accession into the CPTPP could lead to 99.9 per cent of UK exports to CPTPP members being eligible for tariff-free trade (Matsuura, 2021). The significance of the UK’s accession 18 goes beyond strict trade interests at a time of creeping protectionism. If successful, as the first non-founding member to join the CPTPP, UK firms’ digital reach is expected to expand under CPTPP digital trade rules.

Accelerating Asia as a key export region

More, however, needs to be done if the UK is to seize Asia’s full trade potential.

Looking ahead, the new leadership will need to focus on tackling the obstacles to trade with Asia’s economies in order to support overall economic resilience given the UK’s significant trade and investment openness. This is particularly important in light of the spectrum of growing economic and geopolitical risks, both globally and in the Asia region. Bolstering broader economic ties will be essential.

Resilience and openness to Asia should be the dual policy goal for UK trade policy. These can be maintained if competitiveness, coordination and flexibility are the key policy levers that are employed to expand the UK’s trade pathways.

Increased competitiveness to underpin UK exports will be key to shifting UK trade with Asia, and its external deficit position with the region. In order to do so, its export strategy will need to focus on broader economic diversification away from the EU to Asia’s most dynamic economies. The strategy of ‘made in the UK, sold to the world’ (DIT, 2022) will require more than a competitive sterling exchange rate. Initiatives such as providing end-to-end support for export finance and reducing costs will be essential in facilitating trade with the £9 trillion Asia-Pacific region, following UK entry into CPTPP.19 The recently announced Developing Countries Trading Scheme, which covers 65 countries, and platinum partnerships with lower and middle-income commonwealth countries,20 which will reduce import (and some producer input) costs – but could also increase the UK trade deficit. Additionally, the new rules would not extend to other countries that negotiate FTAs with the UK (including India), or to products originated from a number of economies, including Korea and Japan (Mendez-Parra, 2022). More targeted measures are needed to bolster exports with Asia, if resilience is to be the overriding priority.

Coordination between domestic policy and trade policy will benefit UK exports to Asia. The government’s own impact assessments showed that trade deals with major agricultural exporters, like Australia, would reduce UK farming output (DIT, 2021). This underscores the need for better coordination between domestic and trade policy with emerging markets in Asia – and improved monitoring of the impact of trade deals. Additionally, stronger and coordinated global value chains with Asia would increase resilience and productivity (D’Aguanno et al., 2021) – a rise in re-shoring would impose economic costs without significantly increasing resilience (ibid). Fostering broader economic growth as an open and integrated economy need

Targeted and diversified trade with ASEAN is essential given the likely divergence in UK growth prospects when it comes to ASEAN and China. Digitalisation of trade and trade in digital goods and services, and in ICT, could widen the broader divide between UK-ASEAN trade and UK-China trade. A key way in which the UK can achieve a paradigm shift with its Asian partners is through actively diversifying its trading relationships beyond the luxury consumer goods and automobile sectors.

The UK is open in its financial, investment and trade positions, but when it comes to trade, its chronic external deficits mean policymakers continue to manage a structural deficit position. The depreciation in the pound sterling could help boost overall competitiveness, but export growth could be significantly supported by areas of dynamism in Asia’s growing economies.

Southeast Asia and China remain less dominant export markets for the UK when compared to the EU, by a large margin. Successive UK administrations have, however, laid the foundation for new trade agreements and economic cooperation with Asian markets. Now, it will be important for the new leadership to build on these foundations, and accelerate trade with Asia to ensure ‘Global Britain’ succeeds.

NOTES

1. Research conducted for The Independent by the University of Sussex UK Trade Policy Observatory: UK’s Brexit losses more than 178 times bigger than trade deal gains | The Independent

2. The UK withdrew from the European Single Market and the European Customs Union on 31 December 2020.

3. https://www.gov.uk/government/news/uk-and-new-zealand-sign-comprehensive-trade-deal

4. https://www.gov.uk/government/news/new-bill-to-enable-implementation-of-australia-and-new-zealand-trade-deals

5. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1091688/united-states-trade-and-investment-factsheet-2022-07-20.pdf

6. https://www.gov.uk/government/publications/uk-and-indiana-trade-and-economic-memorandum-of-understanding/memorandum-of-understanding-on-economic-cooperation-and-trade-relations-between-indiana-and-the-united-kingdom

7. World Bank World Development Indicator database.

8. International Monetary Fund projections indicate a more than doubling of the UK current account deficit in 2022 to 5.5 per cent of GDP (from 2.5 per cent in 2021).

9. ASEAN is comprised of Indonesia, Malaysia, Philippines, Singapore, Thailand, Brunei Darussalam, Viet Nam, Lao PDR, Myanmar and Cambodia.

10. ASEAN Secretariat (2021) “ASEAN Key Figures 2021” Jakarta, Indonesia, December 2021.

11. https://www.gov.uk/government/publications/uk-indonesia-partnership-roadmap-2022-to-2024/uk-indonesia-partnership-roadmap-2022-to-2024

12. https://www.gov.uk/government/news/uk-viet-nam-joint-statement

13. https://indbiz.gov.in/india-to-transform-into-a-us30-trillion-economy-by-2050-gautam-adani/

14. https://www.gov.uk/government/news/uk-launches-india-negotiations-to-kick-off-5-star-year-of-trade

15. https://committees.parliament.uk/committee/448/international-agreements-committee/news/172275/ukindia-trade-deal-must-not-be-rushed-as-securing-improvements-to-indias-business-environment-is-key/

16. The GCC is comprised of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE.

17. https://www.gov.uk/government/news/hundreds-of-scottish-businesses-set-to-benefit-as-uk-launches-trade-deal-with-gulf-nations

18. https://www.gov.uk/government/news/trade-secretary-secures-major-trade-bloc-milestone-ahead-of-asia-visit

19. https://www.gov.uk/government/news/britain-launches-negotiations-with-9-trillion-pacific-free-trade-area

20. https://www.gov.uk/government/news/new-trading-scheme-cuts-tariffs-on-hundreds-of-everyday-products

REFERENCES

Asia House (2022), “UK-GCC Free trade negotiations: Obstacles and opportunities.” Asia House, 9 May 2022.

Asia House (2021a), “Vietnam’s investment shift could boost its resilience” Asia House, 27 August 2021.

Asia House (2021b), “Liz Truss outlines UK’s trade prospects in Asia” Asia House, 2 September 2021.

Bank of England (2021), “Financial Stability Report – December 2021” Bank of England, December 13, 2021.

Cesa-Bianchi, A., Dickinson, R., Kosem, S., Lloyd, S., Manuel, E. (2021), “No economy is an island: how foreign shocks affect UK macrofinancial stability” Quarterly Bulletin 2021 Q3, Bank of England.

D’Aguanno, L., Davies, O., Dogan, A., Freeman, R., Lloyd, S., Reinhardt, D., Sajedi, R., and Zymek, R., (2021), “Global value chains, volatility and safe openness: is trade a double-edged sword?” Financial Stability paper No. 46., Bank of England, 15 January 2021.

DIT (2022), “Department for International Trade annual report and accounts 2021 to 2022” Corporate Report, Department for International Trade, 29 July 2022.

DIT (2021), “Impact Assessment of the Free Trade Agreement between the United Kingdom of Great Britain and Northern Ireland and Australia” Department for International Trade, 2021.

FCDO (2022), “Plan of action to implement the ASEAN-United Kingdom Dialogue Partnership (2022 to 2026)” Policy Paper, August 4, 2022, Foreign, Commonwealth & Development Office.

Frankel, J. A., and D. Romer. 1999. ‘Does Trade Cause Growth?’ American Economic Review 89 (3): pp.379–399.

Lambe, J. (2022), “The UK and ASEAN: A New Stage in Indo-Pacific Engagement” RUSI, 24 May 2022.

Matsuura, H., (2021), “Why joining the CPTPP is a smart move for the UK” Chatham House, 19 March 2021.

Mendez-Parra, M. (2022), “The UK’s new Developing Countries Trading Scheme: a welcomed change?” Overseas Development Institute, 17 August 2022.

Milligan, E. (2022), “Truss Says UK Should Crack Down on Chinese Firms Like TikTok” Bloomberg, 25 June 2022.

Mireles-Flores, L., (2022) “The Evidence for Free Trade and Its Background Assumptions: How Well-Established Causal Generalisations Can Be Useless for Policy” Review of Political Economy, 34:3, pp. 534-563

Parker, G. (2022), “Rishi Sunak and Liz Truss talk tough on China in race for No 10” Financial Times, 25 July 2022.

Parkin, B., and Reed, J., (2022), “India and UK to seal trade deal in the ‘next few months’, minister says. Financial Times, 7 July 2022.

UKTPO (2019), “The Future of UK-US Trade: An Update” UK Trade policy Observatory, Briefing paper 34, July 2019.

Winters, L.A., and Larbalastier, G., (2021), “The UK’s New Trade Agreements: Curb Your Enthusiasm” UK Trade Policy Observatory, 8 November 2021.