Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

There have been notable shifts in Asian economies’ ability to foster green finance and digitalisation in Q1, according to the latest Asia House Economic Readiness Indices.

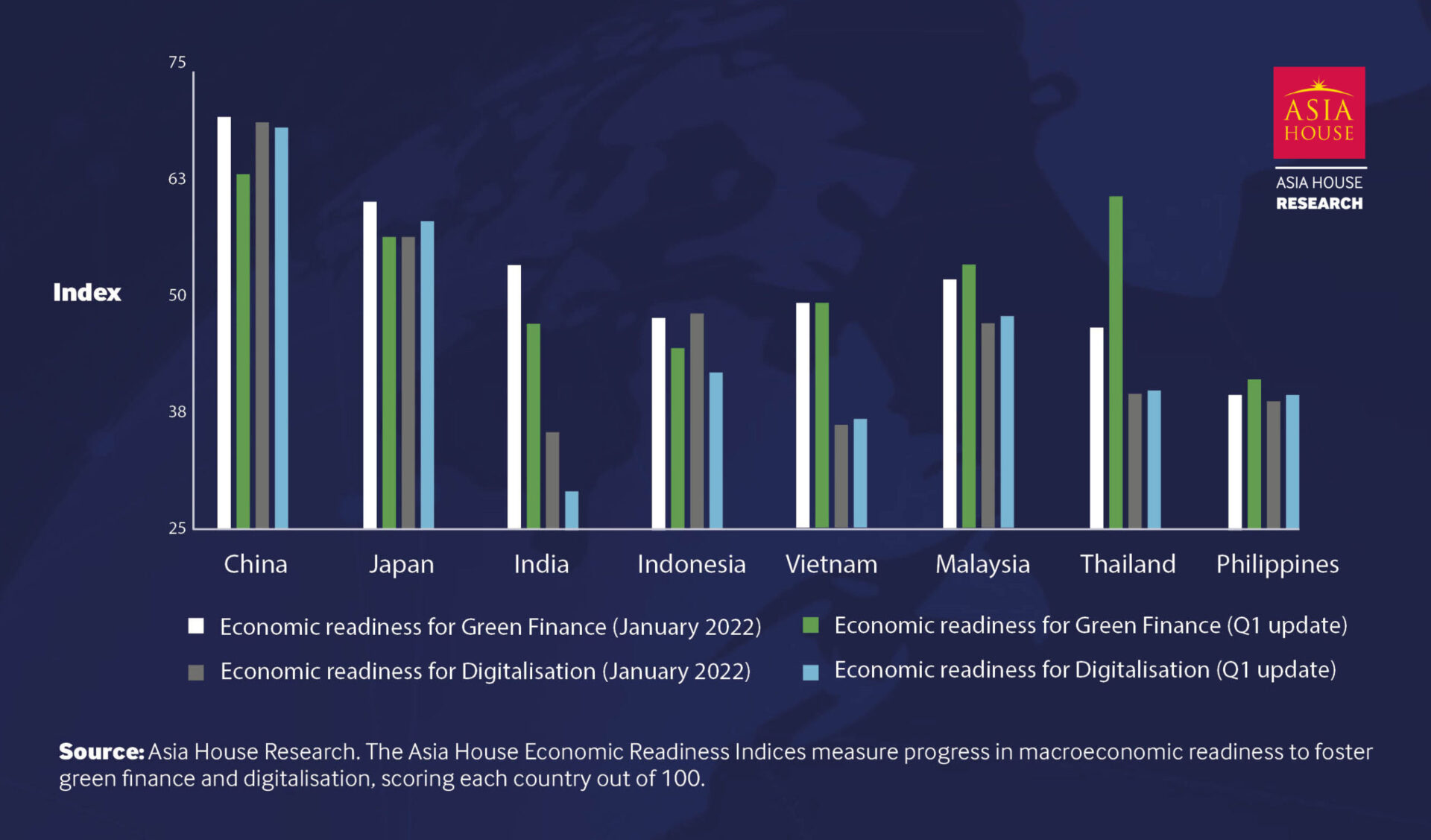

The quarterly update to the indices – which were originally launched in January 2022 – shows a mixed picture across Asia, with the Ukraine crisis and economic scarring from COVID-19 hindering the development of green finance and broader digitalisation in the region. While China and Japan showed resilience across the green finance and digitalisation indices, India saw significant reversals in both. Thailand was the biggest mover, jumping from 48 to 64 in the green finance index.

Asia finds itself at an important crossroads with its economies poised to transition to higher levels of income, innovation, and resilience – despite the ongoing challenges of the COVID-19 pandemic and developments in Ukraine. The Asia House economic readiness indices for green finance and digitalisation were launched in January 2022 to gauge progress in the region’s eight core economies[1] – the notable greenhouse gas emitters and those most vulnerable to the climate crisis. This Asia House Research briefing presents the findings from the first quarterly update of the indices for green finance and digitalisation (Figures 1 to 3).

Quarterly indications suggest that the knock-on impacts from current developments in Ukraine, alongside economic scarring linked to the COVID-19 crisis (particularly in the form of higher debt and weaker reserve dynamics), continues to hinder macroeconomic readiness for green finance. Scarring continues to coincide with a shortfall in appropriate monetary accommodation in Southeast Asia. Asia’s exchange rate weakness (and intermittent financial volatility) will continue amid developments in Ukraine and associated energy market volatility. Cross-border investment has shown signs of strength in China, Japan and India but has been weaker than expected in Southeast Asia.

Quarterly indications of economic readiness for digitalisation have been mixed. There has been resilience and strength in China, which has contrasted with comparatively weaker developments elsewhere in Asia. An illustration of this has been trade in ICT goods exports and digital connectivity. China’s sub-indices strengthened while India’s declined on both fronts. Vietnam’s resurgent strength in ICT goods trade was notable and boosted its index reading. The investment climate has been downcast, with the investment share of GDP weaker across all country indices.

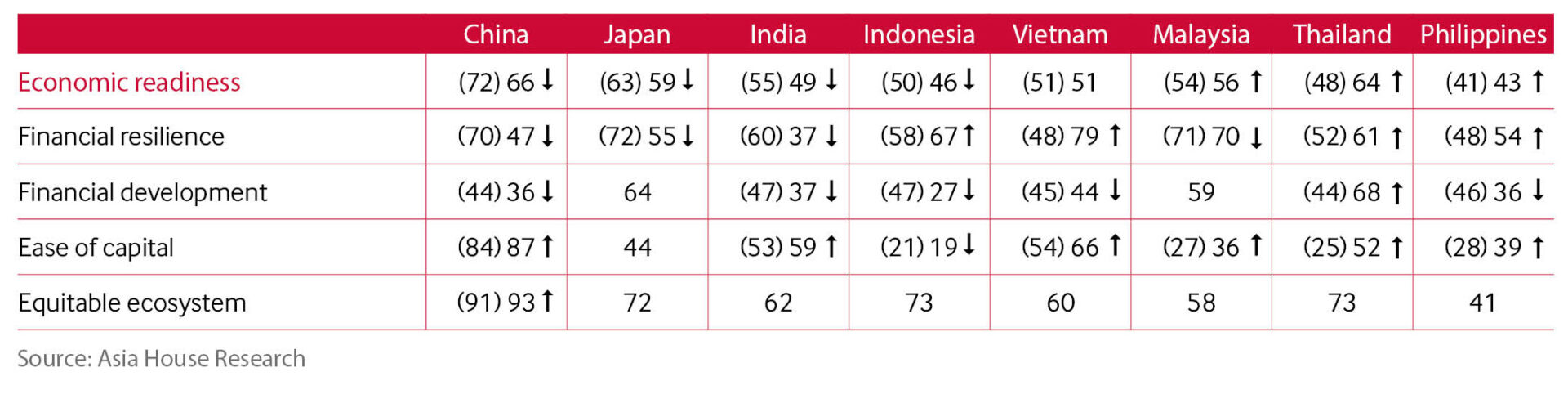

Figure 1. Asia House Economic Readiness Index scores for Green Finance

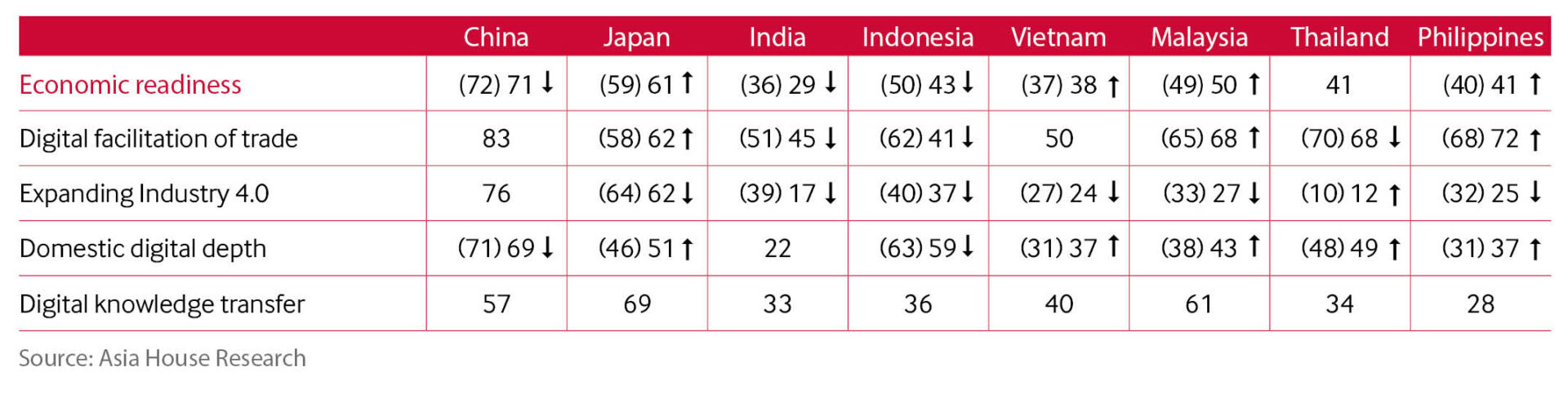

Figure 2. Asia House Economic Readiness Index scores for Digitalisation

Figure 3. Asia House Economic Readiness scores for Asia-8

Economic readiness in green finance and in digitalisation continues to vary markedly across Asia’s major economies. Pervasive economic uncertainty, including from the COVID-19 crisis, and more recently, the conflict in Ukraine, has continued to impact economies through multiple pathways.[2]

China

Readiness readings for green finance and digitalisation have largely shown resilience. Accommodative monetary policy and strength in FDI have offset recent financial volatility (with the latter reflected in slower reserve accumulation and renminbi weakness, contributing to a decrease in China’s financial resilience metric). China’s digital readiness scores, meanwhile, were supported by resilience in ICT goods exports.

Japan

Readiness readings have been supported by the Bank of Japan’s monetary accommodation, domestic credit growth and resilient FDI. The depreciation in the yen exchange rate, due in part to terms-of-trade effects from oil price developments, has been a key source of uncertainty and led to a notable drop in Japan’s financial resilience score. However, Japan’s digital readiness readings were boosted by medium and high-tech manufacturing and ICT import demand.

India

Readiness readings showed a notable deterioration in both green finance and digital readiness. Weaker than expected portfolio investment, a rise in non-performing loans, alongside higher real rates accounted for the indices’ falls. India’s digital readiness was negatively impacted by developments in ICT trade, domestic investment and subdued improvement in broadband coverage, reflected in the sharp decline in India’s ‘Expanding Digital 4.0’ metric.

Indonesia

Readiness readings for green finance were primarily impacted by negative inputs from higher than expected real interest rate developments. However, its green readiness index was buoyed by growth in market capitalisation and inward investment. Indonesia’s digital readiness was negatively impacted by weakness in ICT trade and subdued improvement in broadband coverage.

Vietnam

Readiness scores for green finance and for digitalisation showed broad-based resilience and strength. Sub-indices for green finance showed strength in portfolio (and foreign direct) investment and in market capitalisation. The rise in real rates and in non-performing loans were offsetting negative factors. Vietnam’s digital readiness improved on account of particular strength in domestic investment and ICT trade.

Malaysia

Readiness scores for green finance were driven by broad-based strength in monetary accommodation, reserve developments, portfolio (and foreign direct) investment and market capitalisation. Digital readiness also improved and, as with several other economies in Southeast Asia, was driven primarily by an improvement in ICT trade and broadband coverage.

Thailand

Readiness scores for green finance showed the largest improvement of all of the economies, taking its overall reading to second position following China’s score. There was improvement in all of its sub-indices with particular strength in market capitalisation and a rebound in portfolio and foreign direct investment, contributing to a strong improvement in the Financial Development metric. Thailand’s digital readiness performance was primarily driven by greater broadband coverage.

Philippines

Readiness scores for green finance were driven in large part by resilience in its reserve dynamics and monetary accommodation. Notably, the uptrend in non-performing loans was a mitigating factor in the improvement of the overall index. The Philippines’ digital readiness was driven by an improvement in broadband coverage and mobile connectivity.

The middle months of the year could see further deterioration in Asia’s economic capacity to promote green finance and digitalisation. Economic scarring from COVID-19, geopolitical conflict and the continued rise in energy and commodity prices is likely to create persistent uncertainty. This, in turn, will hurt economic growth significantly (through both consumption and investment) as well as cross-border trade. Crucially, uncertainty about the outlook is also likely to limit policymakers’ ability to cushion against the most recent energy price shock; and, by consequence, impinge on their ability to promote sustainable green finance. On this basis, a further deterioration in the next indices update, due in July 2022, is more than likely, particularly for the resource-dependent economies.

[1] The eight countries are China, Japan, India, Indonesia, Vietnam, Malaysia, Thailand and the Philippines.

[2]For further details on the composition of the Asia House Economic Readiness Indices, please see the January 2022 issue of the Asia House Annual Outlook.

FIND OUT MORE ABOUT ASIA HOUSE RESEARCH