Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

As 2022 comes to a close, what has been termed the ‘era of shocks’[1] comprising the pandemic, the Ukraine conflict and the cost of living crisis is likely to continue into 2023. More restrictive financial conditions, including through US dollar appreciation, are also still at the early stages of impact on emerging market economies, given reserve buffers.

The combination of systemic shocks, the global economic slowdown and monetary tightening could catalyse further triggers of instability. An illustration of this could be the need for a large institutional or sovereign bailout in the next year. Resilience amid multiple, frequent and interconnected shocks is likely to be low.

Discussions of multilateral financing windows to help countries with basic necessities are only likely to be the start of a raft of national interventions and policies. This update of Asia House Economic Readiness Indices[2] indicates that financial resilience has declined in Asia. This could have a knock-on impact on climate resilience and digital readiness.

Asia continues to find itself both managing acute economic shocks and its longer-term goal of transition to higher levels of innovation, resilience and sustainability. Its challenges now include a growing inflationary spiral and monetary tightening. This briefing presents the three key findings from the third-quarter update of the indices for green finance and digitalisation (Figures 1 to 3).

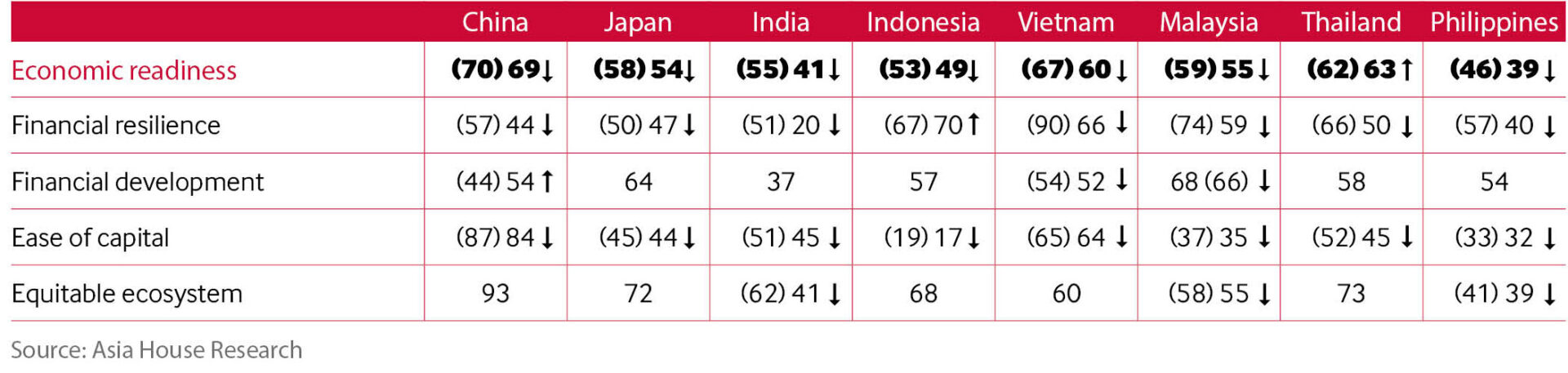

Figure 1: Asia House Economic Readiness Index scores for Green Finance

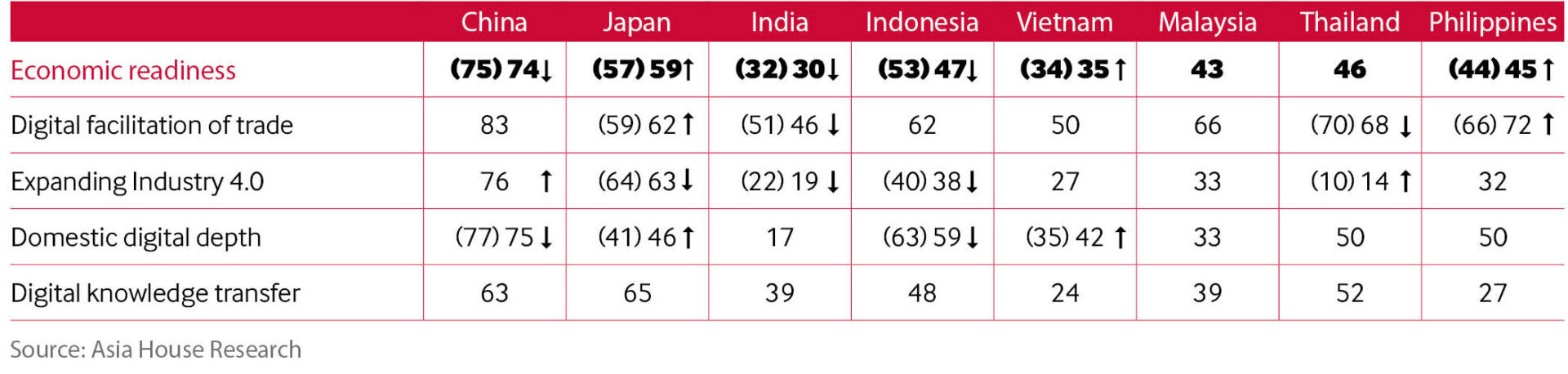

Figure 2: Asia House Economic Readiness Index scores for Digitalisation

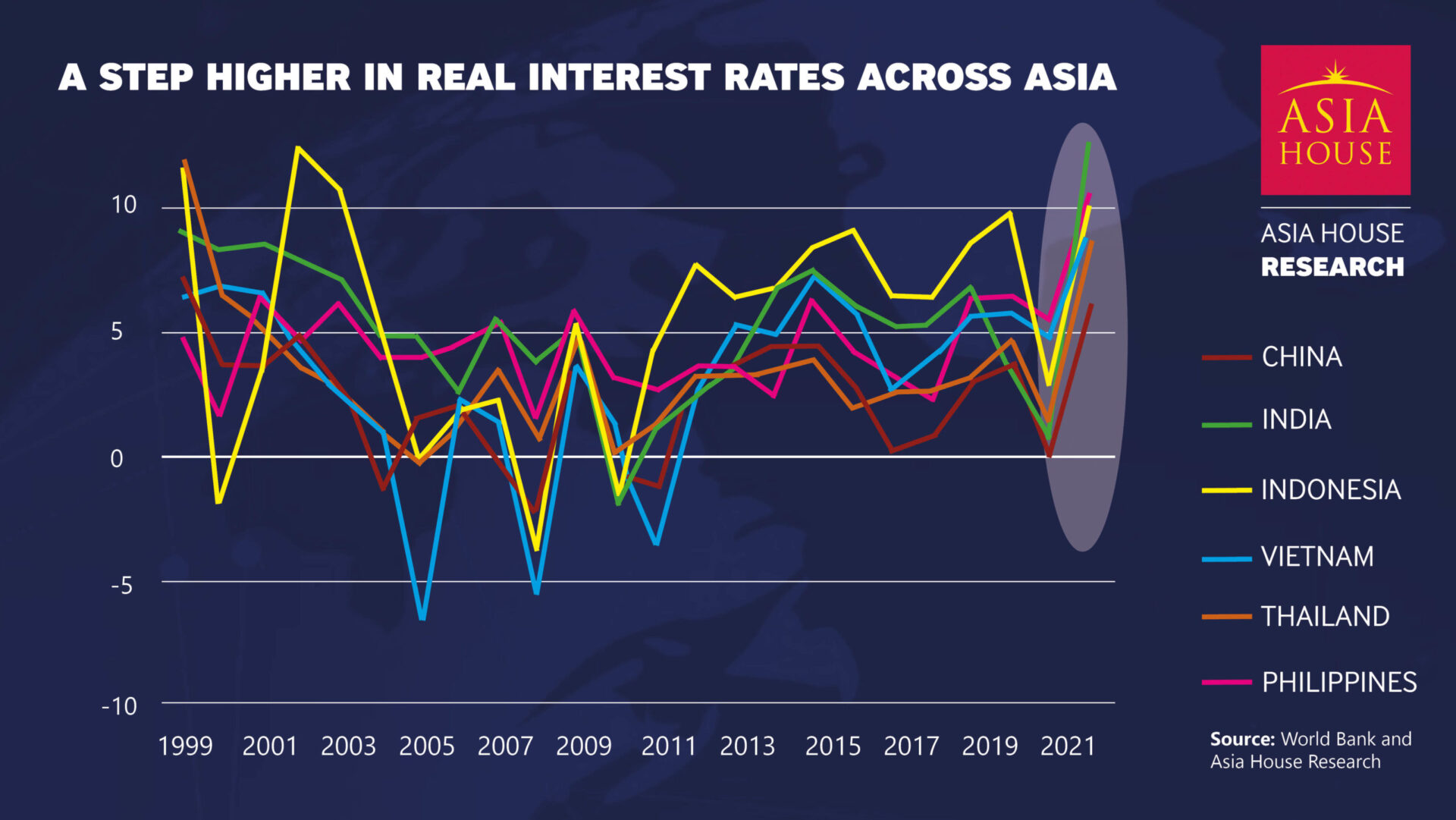

Figure 3: Real interest rates

The divergence across Asia’s economic readiness indices in green finance and in digitalisation has diminished owing to the broader economic downturn. Pervasive economic uncertainty, including from the acceleration in and composition of inflation, and global monetary tightening, will continue to impact economies through multiple pathways.[3]

China readiness readings for green finance and digitalisation have shown deterioration in the light of weakness in reserve accumulation and in the renminbi; Digitalisation efforts showed comparative resilience amid a deal signed with Malaysia.

Japan readiness readings for green finance have deteriorated owing in part to the pronounced depreciation in the yen exchange rate and the rise in real interest rates. The digital policy push should continue to improve digital readiness readings.

India showed the largest decline in financial resilience and ease of capital when it comes to its readiness for green finance. On the digital front, where India is the worst performer, the degree to which the digital economy is scaled up will be of importance.

Indonesia readiness readings for green finance and digitalisation were mixed, with strength in financial resilience but declines in digital readiness. Indonesia’s green readiness index deteriorated, notwithstanding its domestic resource endowments.

Vietnam readiness scores were mixed with broad declines in its green readiness index but relative resilience in its digital readiness. Vietnam’s comparative strength in its growth performance augurs well for sentiment in relation to its green ecosystem.

Malaysia readiness scores for green finance saw broad declines owing to weaker reserves and a depreciating exchange. Malaysia’s new digital telecommunications deal with China, including 5G deployment and cybersecurity, has been of note.

Thailand readiness scores continued to show comparative resilience after having exhibited strength in the first half of 2022. Policies aimed at expediting digitalisation have focused on the deployment of 5G technology across multiple sectors.

Philippines readiness scores were significantly impacted by a drop in financial resilience. Encouragingly, digiitalisation efforts have been boosted by new technology platforms that aim to digitalise the country’s MSMEs.

The start of 2023 could stand in stark contrast to the general resilience seen in Asia for most of 2022. It may be, for example, that financial volatility becomes deeper and more broad-based impacting the depth, breadth and scale of Asia’s financial market development. This would be pivotal in that it would limit countries’ green ecosystems and domestic digital economies. The continued knock-on impact from the Ukraine crisis, now coupled with more broad-based and faster global monetary tightening, will heighten Asia’s headwinds too.

FIND OUT MORE ABOUT ASIA HOUSE RESEARCH

Notes

[1]CGD Talks: Compound Crises Call for Decisive Action: https://www.imf.org/en/News/Articles/2022/09/14/tr091322-cgd-transcript

[2]The Asia House Economic Readiness Indices for green finance and digitalisation were launched in January 2022 to gauge progress in the region’s eight core economies that include China, Japan, India, Indonesia, Vietnam, Malaysia, Thailand and the Philippines.

[3]For further details on the composition of the Asia House Economic Readiness Indices, please see the January 2022 issue of the Asia House Annual Outlook.