Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Asia House Middle East Associate Freddie Neve takes stock of recent green policy developments in the region, and argues that more investment is needed to support the Gulf’s vision for global decarbonisation.

Freddie Neve

Freddie Neve

Asia House Middle East Associate

Freddie leads the Asia House Middle East Programme, convening briefings and events with leading business and policy figures and conducting research focused on the region.

Key takeaways

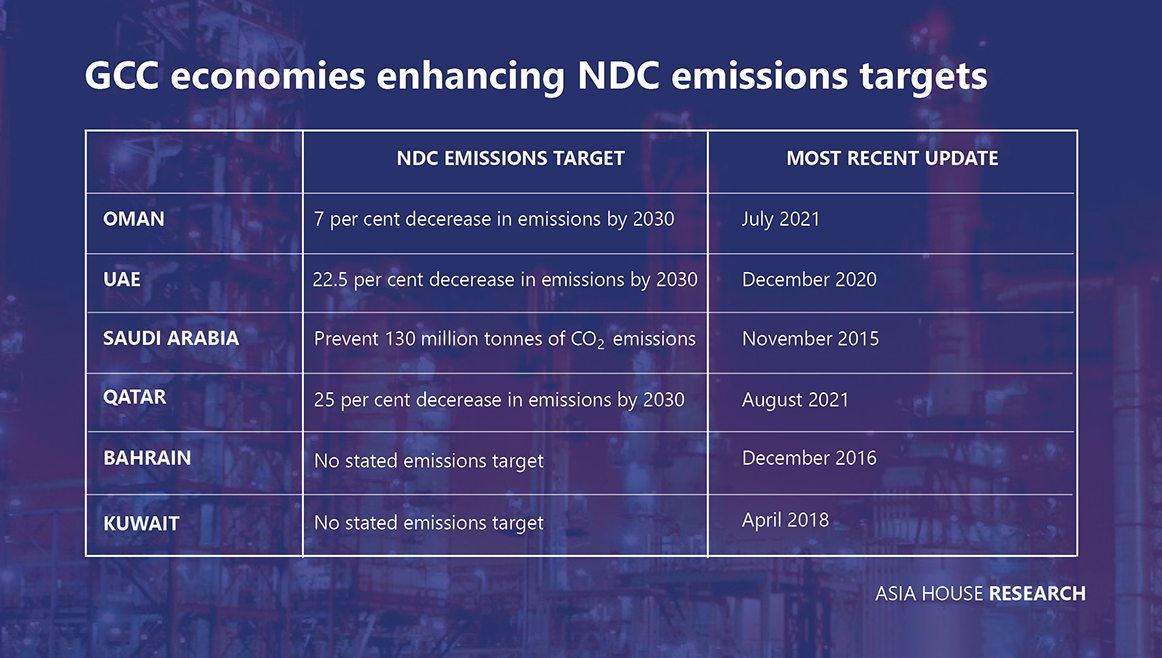

The past year has seen the Gulf states enter a new era of climate diplomacy. The UAE, Bahrain, and Qatar have for the first-time appointed climate change envoys and a UAE-led regional summit brought together several leaders from the Middle East and North Africa (MENA) to accelerate action on climate change. New Nationally Determined Contributions (NDC) under the Paris climate accords have also been announced, with Oman, the UAE, and Qatar committing to reduce greenhouse gas emissions by 7 per cent, 23.5 per cent, and 25 per cent respectively by 2030.

Table 1

Saudi Arabia, the region’s largest oil producer, has launched two ambitious climate change initiatives, ‘The Saudi Green Initiative’ (SGI) and ‘The Middle East Green Initiative’ (MGI). The latter aims to reduce Middle East carbon emissions by 60 per cent by 2030 and both initiatives will see the delivery of the world’s largest afforestation scheme, which would see 50 billion trees planted.

There is recognition among Gulf leaders that climate change could devastate their countries. Research by the Max Planck Society notes that Middle Eastern countries’ summer temperatures could rise by four degrees by around 2050 if the average global temperature increase is limited to two degrees. These temperature increases could potentially destabilise regional food and water security – and fuel conflict. Increased desertification, dust storms, and coastal erosion could also reduce tourism and investment into the region, undermining the Gulf states’ economic strategies.

The Gulf states are increasingly looking to place themselves on a more environmentally sustainable footing through investment in renewable energy; dedicating government resource to fostering international and intraregional dialogue that seeks solutions to climate change; and exploring more stringent targets towards net-zero emissions.

August 2021 alone saw the following developments:

GCC governments could announce even more ambitious climate change targets prior to November’s COP26 meeting in Glasgow. This month, Saudi Arabia announced it will host both the ‘Saudi Green Initiative Forum’ on 23 October and ‘The Middle East Green Initiative Summit’ on 25 October. Policymakers and sustainable investors will be watching these events closely for greater clarity and transparency regarding how Saudi Arabia will implement its SGI and MGI initiatives, but these events may also provide the stage for more ambitious climate change targets, with the webpage for the Middle East Green Initiative Summit promising to introduce the Middle East’s first pact on climate change. US special climate envoy John Kerry recently expressed optimism following a trip to Saudi Arabia that the Kingdom could ultimately commit to a net-zero emissions target around 2050.

The GCC’s other major economies may also be close to announcing more stringent climate commitments. Media has reported that the UAE could be planning to set a net-zero carbon emissions goal, possibly pledging to reach this target by 2050. The UAE is bidding to host COP28 in 2023, so strengthening its climate change targets could improve its candidacy. Qatar, too, has also recently begun exploring pathways towards a net-zero future; joining Saudi Arabia, Canada, Norway and the United States in April 2021 to establish the ‘Net-Zero Producers Forum’ to develop net-zero emission strategies, including methane abatement and the development of CCUS. Finally, Oman’s second NDC submitted in August 2021 notes the country’s upstream oil and gas sector is evaluating a target of zero emissions by 2050.

The Gulf states are serious about developing their renewable energy sector and reducing domestic emissions. However, their vision for global decarbonisation is one where hydrocarbons remain a central part of the global energy mix, but with the negative environmental impact of their emissions reduced by Carbon Capture, Utilisation, and Storage (CCUS) technologies.

The Gulf states’ determination to continue exporting hydrocarbons is underscored by Saudi Arabia’s Energy Minister Abdulaziz bin Salman’s recent pledge to drill “every last molecule” of oil in Saudi Arabia, as well as recent announcements by major energy companies such as Abu Dhabi National Oil Company (ADNOC), Kuwait Oil Company, and Aramco, indicating production increases.

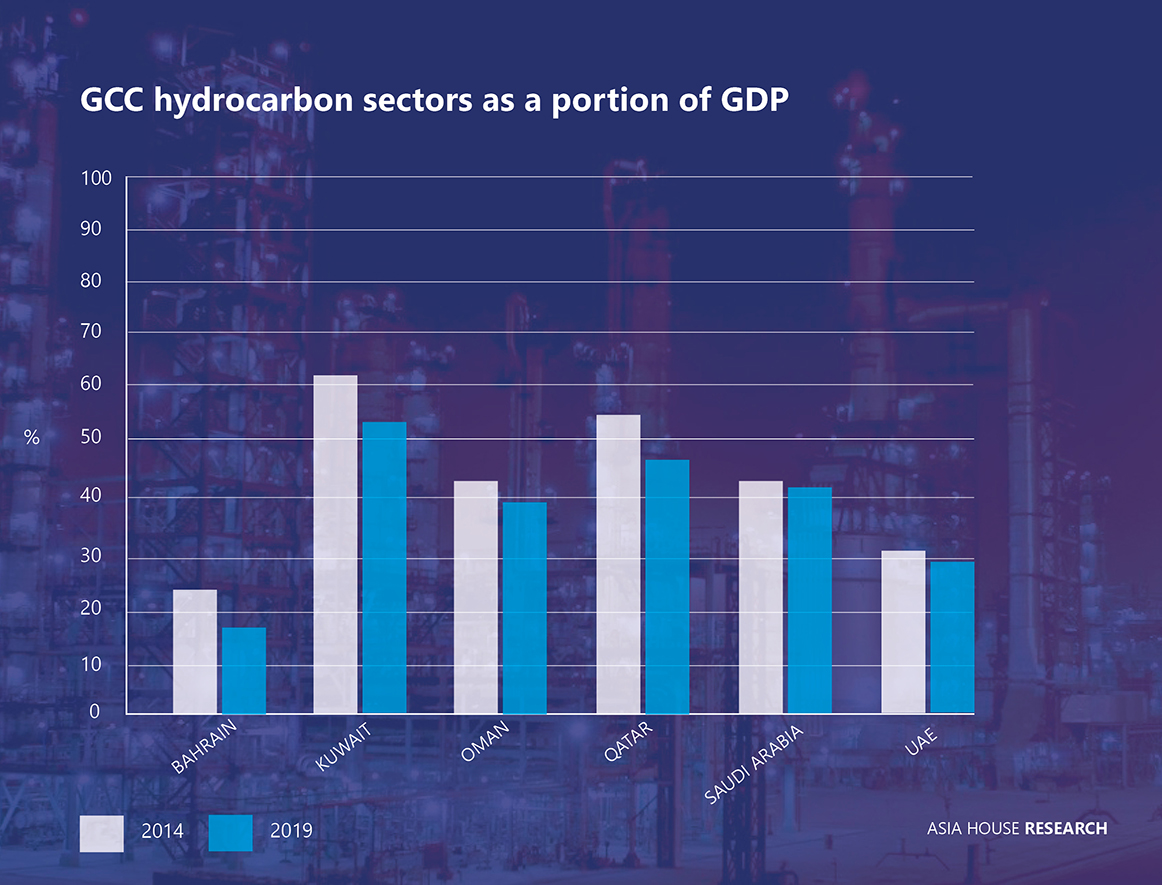

Ultimately the Gulf states remain reliant on fossil fuel exports. While hydrocarbon GDP as a proportion of overall GDP has declined in all GCC economies between 2014 and 2019, it has not done so significantly.

Figure 1

Source: The World Bank: Gulf Economic Update, August 2021

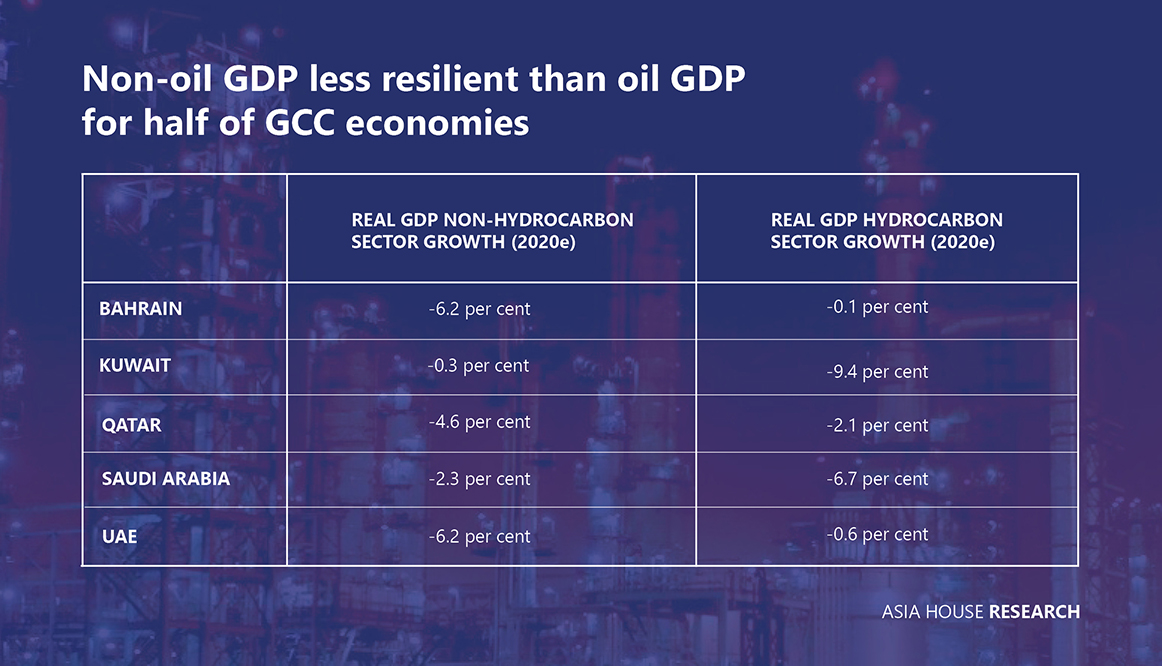

Challenges to economic diversification still remain. For example, World Bank estimates from August 2021 show the UAE, Qatar, and Bahrain experiencing greater economic contraction in their non-hydrocarbon sectors than in their hydrocarbon sectors during 2020 and the COVID-19 pandemic.

Table 2

Source: The World Bank: Gulf Economic Update, August 2021

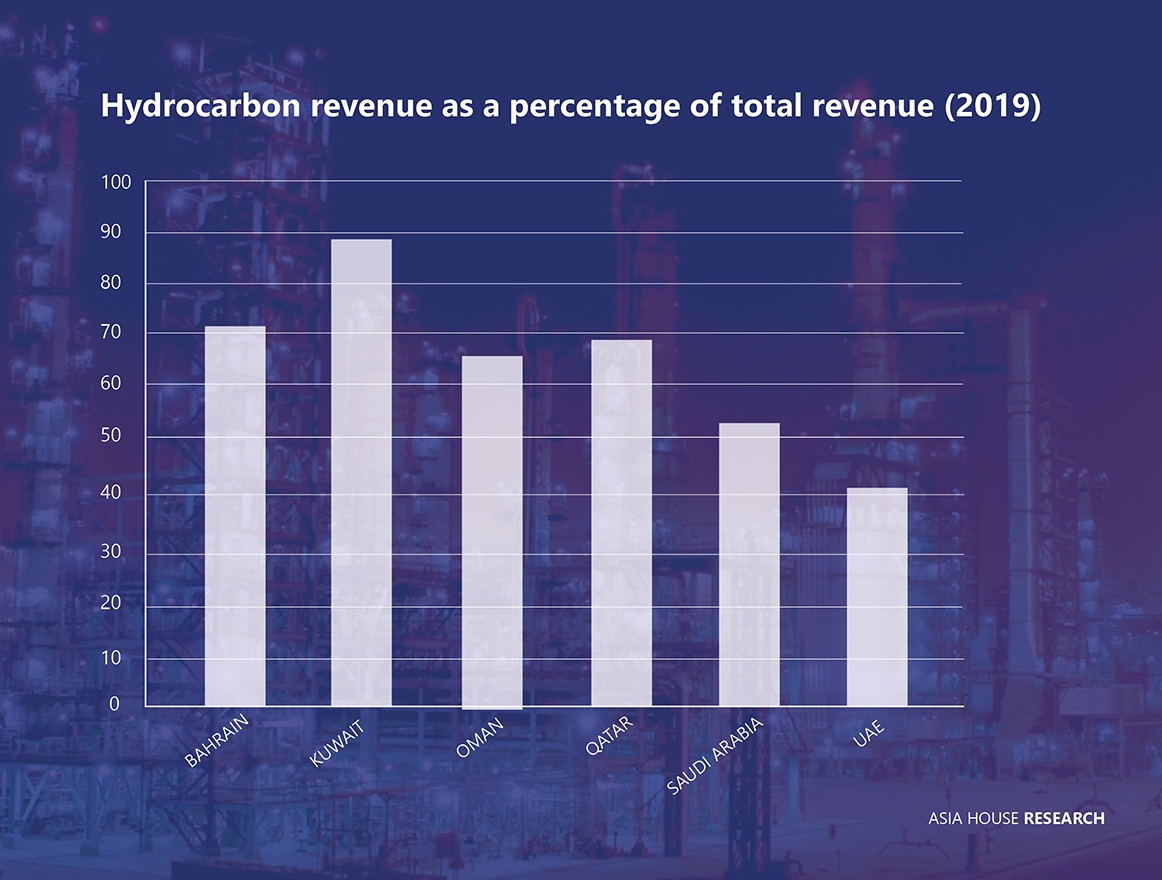

Oil and gas exports are still crucial to meeting GCC revenue targets. As the graph below shows, oil revenues still exceed 60 per cent of total government revenues in Kuwait, Qatar, Oman, and Bahrain, meaning that even with increased focus on economic diversification, the GGC economies could still be dependent on hydrocarbon revenue for the foreseeable future.

Figure 2

Source: The World Bank: Gulf Economic Update, August 2021

Because the GCC is reliant on hydrocarbon revenue, the Gulf states are investing heavily in developing CCUS technologies and working with the international community to accept and promote CCUS as a tool to reduce carbon emissions. One emerging application of CCUS is capturing the CO2 emitted during the transformation of natural gas into ammonia, creating ‘blue ammonia’. Crucially, ammonia is a store of hydrogen and does not emit any CO2 when burned, and therefore could assist other countries with their energy transition.

There remains debate regarding blue ammonia’s environmental impacts and risks. Arguments have been put forward that using CO2 produced by blue ammonia, for enhanced oil recovery, is not as environmentally friendly as storing the captured CO2 underground. Recent scientific research has also expressed concern over the risk of methane leakage during the production process.

Still, the Gulf states and other energy producers argue that blue ammonia can play a crucial role in decarbonisation by providing low-carbon fuel to a range of sectors such as shipping, steel production, and aluminium production. Gulf energy majors are investing heavily in the technology with, for example, ADNOC developing a 1,000 kiloton per annum “world-scale” blue ammonia production facility.

Increasingly, in addition to its investments, GCC governments are demonstrating blue ammonia’s real-world applications. In September 2020, Saudi Arabia sent blue ammonia to Japan in a world-first shipment and in August 2021, Abu Dhabi National Oil Company (ADNOC) announcing three separate sales of blue ammonia to new Japanese customers, Idemitsu, Inpex, and Itochu.

GCC development of CCUS, and its associated technologies, aim to support the hydrocarbon sector, but attempts to do so with a reduced environmental impact. More GCC investment in renewable energy will reduce GCC domestic emissions and lower consumption of its own hydrocarbon resources. This will free more oil and natural gas that could be exported to markets outside the GCC, meaning until CCUS is further adopted at scale, Gulf oil exports will continue to generate CO2 emissions.

Gulf investment into developing renewable energy and increasing commitment to tackling climate change are positive developments that international governments and investors should continue to encourage. But alone this will not prevent Gulf hydrocarbons from being exported to other markets and releasing emissions.

Global oil demand is still rising, with the International Energy Agency (IEA) recently forecasting global demand to increase significantly to 2026. Oil remains central to the global economy, as recently demonstrated by the US calling on OPEC to produce more oil to reduce consumer fuel prices. The Gulf states will not want to forgo any potential revenue from meeting this demand, leading to carbon emissions outside its borders.

GCC investment in CCUS technology aims to reduce domestic emissions and advance the technology so that existing oil customers are persuaded that they can continue purchasing hydrocarbons while maintaining their climate change commitments. But the technology remains under-developed and further research and investment into CCUS technologies, as well as alternative fuels such as blue ammonia, are needed to encourage wider-spread adoption.

Increased demand for blue ammonia can assist with encouraging development in greener forms of the technology such as green ammonia, which is produced entirely from renewables. International governments and Gulf governments should cooperate together to identify opportunities to develop and share knowledge on CCUS, as well as identify projects that could benefit from investment.

There is a need for GCC governments and global financial institutions to elevate the financing and investment of CCUS. The Gulf states themselves are increasingly open to green finance. The value of green bonds issued in the Middle East and North Africa (MENA) region rose from US$2.64 billion in 2019 to US$3.35 billion in 2020. The first half of 2021 also saw green financing for projects in MENA rise by 38 per cent to reach US$6.4 billion. Global financial institutions should work with Gulf states to bring more of these projects to the market, and explore products structured around CCUS and/or blue ammonia investments, while simultaneously working with the Gulf states to develop standards for these technologies to increase investor confidence.

JOIN OUR MAILING LIST to receive Asia House insights, analysis and research direct to your inbox.