Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

The Middle East Pivot to Asia 2022 report presents Asia House’s latest research on trade and investment trends between the Gulf and emerging Asia.

Produced by the Asia House Research and Advisory team, the report aims to help business leaders and policymakers better understand this pivotal shift in global trade, which will have far-reaching economic and geopolitical implications.

KEY FINDINGS

EXECUTIVE SUMMARY

Rapidly expanding ties between the Gulf and Asia are creating a fundamental global shift that will have far-ranging implications for international trade, business and politics.

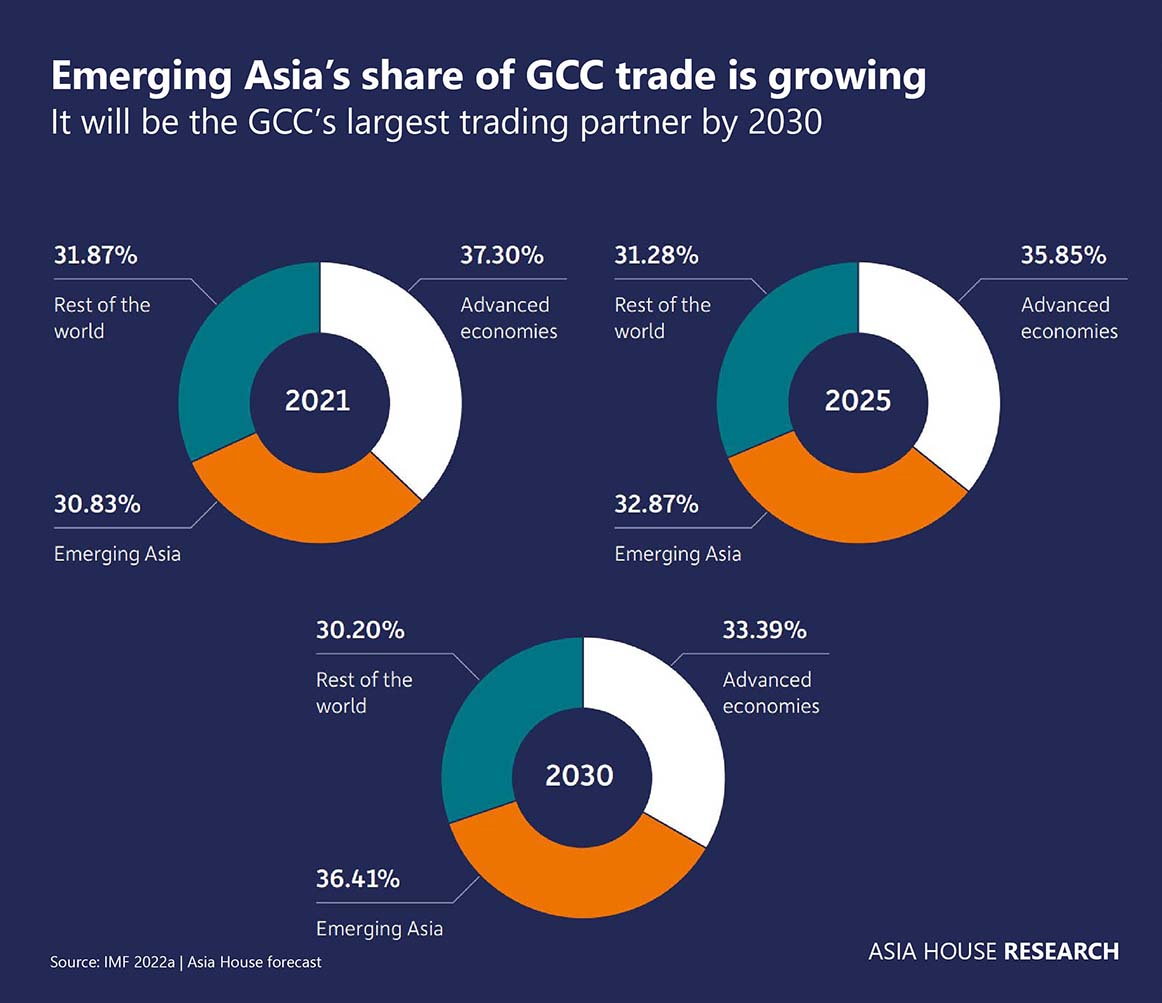

After a quicker recovery than expected from the COVID-19 pandemic, we expect trade between the two blocs to surpass that between the Gulf states and advanced economies by 2028.1

Trade between the Gulf Cooperation Council (GCC)2 and emerging Asia,3 which had dipped from US$320bn in 2019 to US$262bn in 2020, has now recovered to levels not seen since 2014. We expect this trade to continue growing, reaching approximately US$578bn by 2030. As GCC-Asia trade and investment rises, we will see greater bilateral political exchanges and cooperation to protect and expand these investments, making this relationship a significant pillar of global politics.

Our Middle East Pivot to Asia report examines the strengthening economic and political linkages between Asia and the Middle East and underscores the business opportunities these will bring.

Source: IMF2022a | Asia House forecast

Despite a faster-than-expected recovery from the COVID-19 pandemic, global trade faces major obstacles including inflation, global monetary policy tightening, and the Russia-Ukraine conflict.

Oil prices have come off the highs seen during Q2 2022 but remain above the average prices in 2021. This has not only increased the value of GCC-emerging Asia trade in 2022, but also raised revenue for the Gulf states which can be used to drive the Pivot. It supports the economic diversification that has attracted Asian investment in non-oil sectors, as well as Gulf Sovereign Wealth Fund (SWF) investment into Asia.

While there are signs that growth is slowing in China, the economic outlook for Asia and the GCC economies remain broadly positive, with Saudi Arabia expected to be the fastest growing major economy in 2022 (Economist Intelligence Unit, 2022). Inflation, global monetary policy tightening and the Russia-Ukraine conflict have dampened the outlook for global trade and economic growth, but we expect GCC-Asia trade and investment to remain resilient for the following reasons:

China is driving emerging Asia’s trade with the GCC

GCC-China trade has doubled from approximately US$90.6bn to US$180bn between 2010 and 2021 (IMF, 2022a). China is already the biggest trading partner for all GCC economies with the exception of Bahrain, but we are now seeing evidence that GCC-China trade is not just outpacing the GCC’s trade with the US, but also with Western economies as a whole. GCC-China trade has never been higher and 2021 was the first time it had surpassed the GCC’s trade with the US and Euro Area combined. China’s trade with Saudi Arabia exceeded Riyadh’s with the US and Euro Area combined for the first time in 2021. China is increasingly recognising Saudi Arabia as an investment destination.

“In H1 of 2022, no country received more

Belt and Road Initiative (BRI) investment

than Saudi Arabia, at around US$5.5bn

(Wang, 2022a)”

We also expect the UAE’s trade with China to overtake that with Western economies in the future. The difference between UAE trade with China and with the US, the UK, and the Euro Area combined is narrowing, and now stands at approximately US$3.4bn. In 2010, it was US$28bn. While the oil trade is crucial to Sino-GCC ties, cooperation in non-oil sectors, particularly renewables and construction, is growing and aiding the Gulf’s economic diversification. But China’s centrality to the Pivot could also put the latter at risk.

US-China tensions have worsened over the past year and further deterioration could bring pressure on the Gulf states to prioritise or downgrade their relations with one side or the other. The US remains an important security partner for the Gulf states, but China’s status as an important economic partner for the Gulf states is cementing. OPEC’s recent decision to cut production by two million barrels per day (bpd) has led to a deterioration in US-Saudi relations. A prolonged period of poor US-Gulf relations could encourage the Gulf states to enhance ties with China.

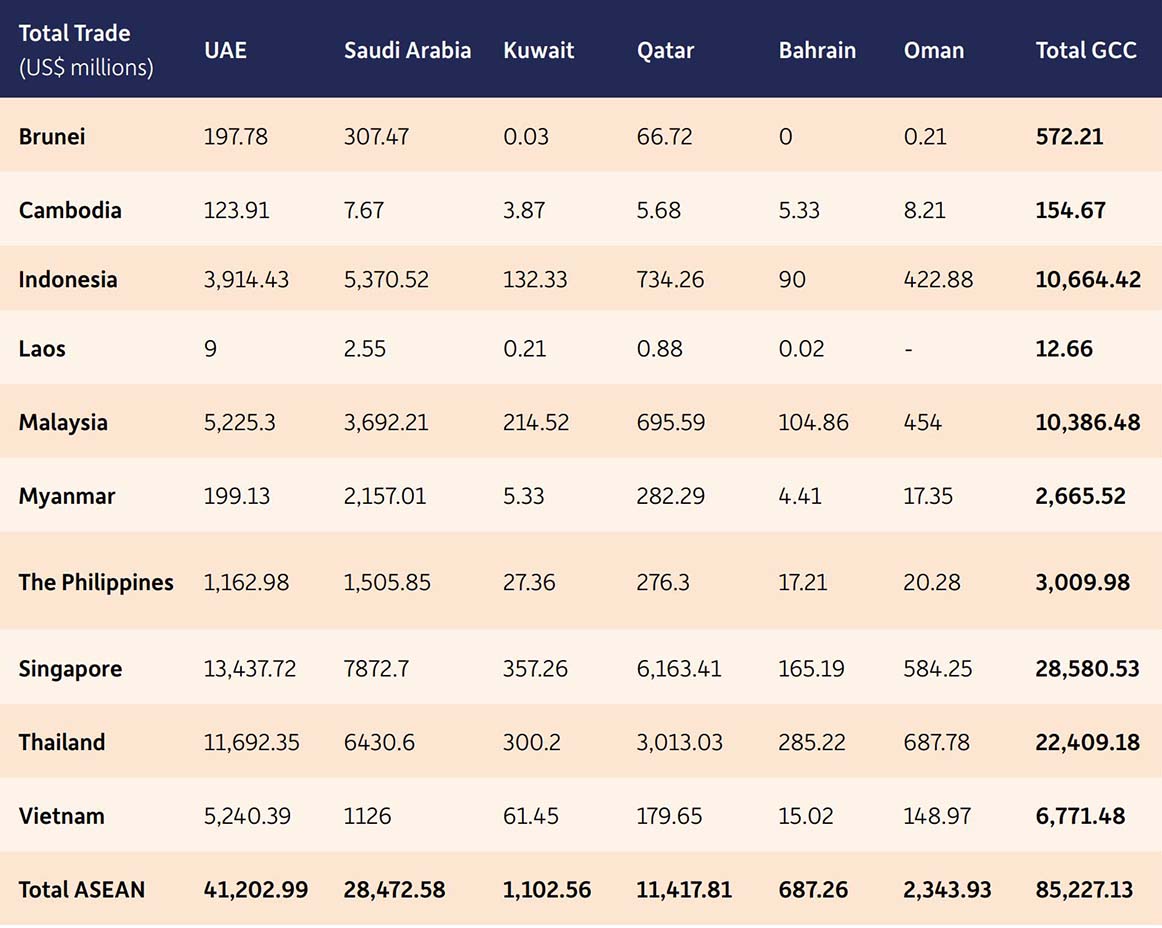

Growing opportunities in GCC-ASEAN trade

This year has seen an uptick in economic and political exchanges between the Gulf states and ASEAN.4 While GCC-ASEAN trade has not grown as quickly as Gulf trade with China and India over the last decade, we expect ties to grow more important with the expansion of ASEAN’s middle classes and good growth prospects for both regions over the next 10 years. There are also natural synergies between ASEAN and Gulf visions for economic growth, with governments in both regions investing in digitalisation, manufacturing, and logistics infrastructure to boost exports.

GCC-ASEAN bilateral trade values (2021)

Source: IMF 2022a

We expect GCC-ASEAN relations to flourish as the UAE’s Comprehensive Economic Partnership Agreement (CEPA) with Indonesia takes effect, as it continues CEPA negotiations with the Philippines, and as Saudi and Thailand restore diplomatic ties after a three-decade hiatus. Gulf Sovereign Wealth Funds (SWFs) are also looking for opportunities in ASEAN, with several investments into start-ups and projects this year, particularly in Singapore and Indonesia.

Oil remains crucial, but GCC-Asia cooperation in non-oil sectors is growing

Hydrocarbons continue to be crucial to GCC trade with Asia and there is a clear link between the oil price and the value of trade. Overall, Asian demand for Gulf hydrocarbons remains robust despite high prices in 2022 and weakened demand in China. Asia’s importance as a source of hydrocarbon revenue for the Gulf states will only grow as its demand expands. Asian investment in the Gulf’s oil industry is strategic and aimed at securing energy supply, with continued interest in extraction and ports. But Gulf economic diversification strategies are opening up new sectors for Asian investment and expertise. As the Gulf states transition away from fossil fuels, GCC-Asian cooperation in this sector will gradually be replaced by investment in sustainability, renewables, and developing alternative energy sources such as hydrogen. Gulf investments in digitalisation, fintech, digital assets, construction, and ports increased GCC-Asia trade in non-oil sectors throughout 2022.

GCC economic and social reform is accelerating and driving the Pivot

Gulf economic and social reform has accelerated over the past year and will be a key driver encouraging Asian investment. The economic shock of COVID-19 prompted Gulf states to speed up their reform programmes, attracting foreign investment and encouraging overseas businesses and their employees to establish bases in the GCC, further driving the Middle East Pivot to Asia. The Gulf states are liberalising their visa requirements and bestowing greater rights and benefits on their expat populations to encourage them to live and work in the GCC and contribute to economic growth over the long-term. New regulations to encourage GCC capital market growth are another key recent development which will foster greater Asian capital flows into the Gulf. The Gulf states are expected to continue their economic and social reform agendas, creating new growth opportunities for both Asian and Western businesses.

Sovereign Wealth Funds look eastwards

Gulf SWFs continue to increase their focus on Asia and are opening new offices there. As these investments grow, Asia will increase in strategic importance to the Gulf states. Interestingly for the Pivot, there has also been an increase in cooperation between Gulf and Asian SWFs in joint investments, for example in the Abu Dhabi Investment Authority (ADIA) and Singapore’s Temasek involvement in GoTo’s pre-Initial Public Offering (IPO) round. India has been an important destination for Gulf SWF investment in 2022 while Saudi Arabia’s Public Investment Fund (PIF) and the Qatar Investment Authority (QIA) increased their focus this year on deal-making in Asia. We expect Gulf SWF interest in Asia to increase as the Pivot develops.

The Middle East Pivot to Asia 2022 report was authored by Freddie Neve, Senior Middle East Associate at Asia House. Further editorial contributions were made by members of Asia House’s Research and Advisory team: Phyllis Papadavid, Zhouchen Mao, and Ayon Dey.

For more information about Asia House’s Middle East expertise and research services, and to enquire about bespoke presentations on the issues covered in the report, please contact Jonathan Smith, Corporate Relations Manager: jonathan.smith@asiahouse.co.uk

NOTES

1. ‘Advanced Economies’ refers to an IMF list of 40 economies, including traditional GCC trading partners such as the US, UK, and Euro Area. Some Asian economies are included in this list, including Japan, Singapore, South Korea, Hong Kong, Macao, Taiwan, Australia, and New Zealand.

2. The GCC is comprised of Saudi Arabia, the UAE, Qatar, Oman, Kuwait, and Bahrain.

3. Emerging Asia’ refers to the IMF’s ‘Emerging and Developing Asia’ list of 34 Asian economies, which includes China, India, and most ASEAN members, but excludes advanced Asian economies such as Japan, Singapore, South Korea, Hong Kong, Macao, Taiwan, Australia, and New Zealand.

4. The Association of Southeast Asian Nations (ASEAN) is a political and economic union of 10 countries. These are Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam. Singapore is classified as an advanced economy, whereas the other economies are categorised by the IMF to be in emerging Asia.