Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

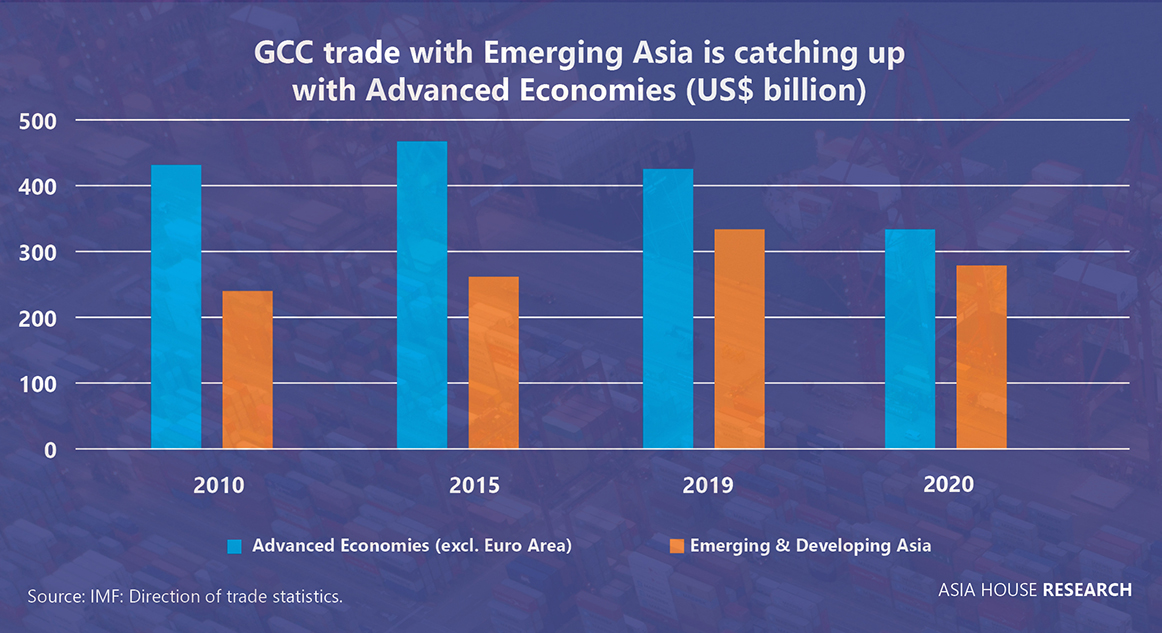

The Gulf’s trade relationships are changing. Between 2010 and 2020, the states of the Gulf Cooperation Council (GCC) saw rapid growth in trade with emerging Asia, in contrast to a slowing of trade with advanced economies.* This Asia House research report explores this key trend, which marks a fundamental shift in the global trade balance.

‘The Middle East Pivot to Asia’ tracks the strengthening economic and political linkages between the two regions. It shows that trade between the Gulf states and emerging Asia has accelerated significantly over the last decade. If underlying growth in bilateral trade and investment between the two regions continues as it has, emerging Asia will become the biggest trading partner for the GCC by 2030, outstripping the GCC’s trade with advanced economies. This could have a profound impact on world trade.

KEY FINDINGS

READ THE FULL REPORT [PDF]

Over the next decade, Asia will take on increased importance as an essential trading partner for the GCC. Growing Asian oil demand, GCC economic diversification, and a rising tendency for GCC sovereign wealth funds (SWFs) to look eastwards, will all drive the Middle East pivot to Asia.

Oil remains central to GCC-Asia trade. Hydrocarbons and their associated products still make up the majority of GCC exports and Asian nations are the main recipients of these exports. Asian nations see Middle East engagement as a key means of securing oil supplies, with Asia frequently investing in Middle East extraction and seeking Gulf expertise in developing refineries at home. While Asian countries are strengthening their green targets, Asian oil demand is expected to continue rising over the next several years. This will encourage further growth in the GCC-Asian economic relationship, with rising oil demand and prices in 2021 supporting this trend.

GCC-Asia trade growth has also been driven by the Gulf states’ economic diversification strategies and megaprojects. These have encouraged Asian investment into new sectors including technology, construction, infrastructure, and renewables. China is a significant source of these funds. Chinese investment into the UAE reached its pre-pandemic peak of US$8 billion in 2018, representing an average annual growth rate of approximately 95 per cent between 2011 and 2018, whereas Chinese investment into Saudi Arabia has also grown at an average annual growth rate of approximately 21 per cent, peaking at US$5.5 billion in 2019. China is now the GCC’s most significant trading partner, with China either the top trading partner or the second-top trading partner for all countries in the bloc.

At the same time, GCC SWFs are increasingly shifting their focus eastwards. This reflects strategic thinking in the Gulf’s capitals and will be a key trend that defines the Middle East pivot to Asia over the next decade. Investments into Asia are on the rise and, importantly, SWFs are also establishing physical offices in these markets in the search for new opportunities. The rise in oil prices from an approximate average of US$40 per barrel in 2020 to multi-year highs in October 2021 at over US$80 per barrel, if sustained, will increase revenue for the Gulf states and encourage increased external investment, including to Asia.

Deepening economic ties have also encouraged deeper political ties, with greater engagement between Middle East and Asian leaders to manage, protect, and grow investments. The Middle East is not looking to weaken its traditionally strong relationship with western powers, but growing commercial opportunities in Asia, increased international investment outflows from Asia, and a desire from some political leaders to strategically hedge between East and West, have led to an increased focus within the Middle East on cultivating ties with Asia.

The Gulf states will need to carefully navigate ongoing US-China tensions. There are some signs that Gulf states are facing pressure from western powers over Chinese investment into sensitive sectors such as security and telecommunications. Gulf ties to China have not yet caused a deterioration in political relations with western economies, but should US-China relations develop into open confrontation, there could be pressure from the US on the Gulf states to deprioritise their relationship with China.

Over the past decade the Middle East pivot to Asia has evolved from being primarily a relationship based on fossil fuel trade to a broader relationship that crosses into multiple sectors and fulfils strategic objectives for both regions. Deepening economic and political ties between the Middle East and Asia will be a key geopolitical trend worth following, and a key driver of global trade over the next decade.

READ THE FULL REPORT [PDF]

* ‘Emerging Asia’ refers to the IMF’s ‘Emerging and Developing Asia’ list of 34 Asian economies, which includes China, India, and the majority of ASEAN members, but excludes advanced Asian economies such as Japan, Singapore, South Korea, Hong Kong, Macao, Taiwan, Australia, and New Zealand. ‘Advanced Economies’ refers to an IMF list of 40 economies, including traditional GCC trading partners such as the US, UK, and Euro Area. Some Asian economies are included in this list, including Japan, Singapore, South Korea, Hong Kong, Macao, Taiwan, Australia, and New Zealand.