Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

In this Asia House Research briefing, Freddie Neve, Middle East Associate at Asia House, explores the state of UK-GCC free trade agreement negotiations, including potential obstacles to an agreement being formed, and what could feature in a future deal.

In this Asia House Research briefing, Freddie Neve, Middle East Associate at Asia House, explores the state of UK-GCC free trade agreement negotiations, including potential obstacles to an agreement being formed, and what could feature in a future deal.

The UK government has staked much political capital on forging an independent trading policy post-Brexit, with free trade agreements (FTAs) central to this strategy. The UK government wants FTAs to cover 80 per cent of its cross-border trade by 2022 and has its sights on the Gulf Cooperation Council (GCC) as a key market to help realise this ambition, recently concluding a public consultation on GCC trade in January 2022.

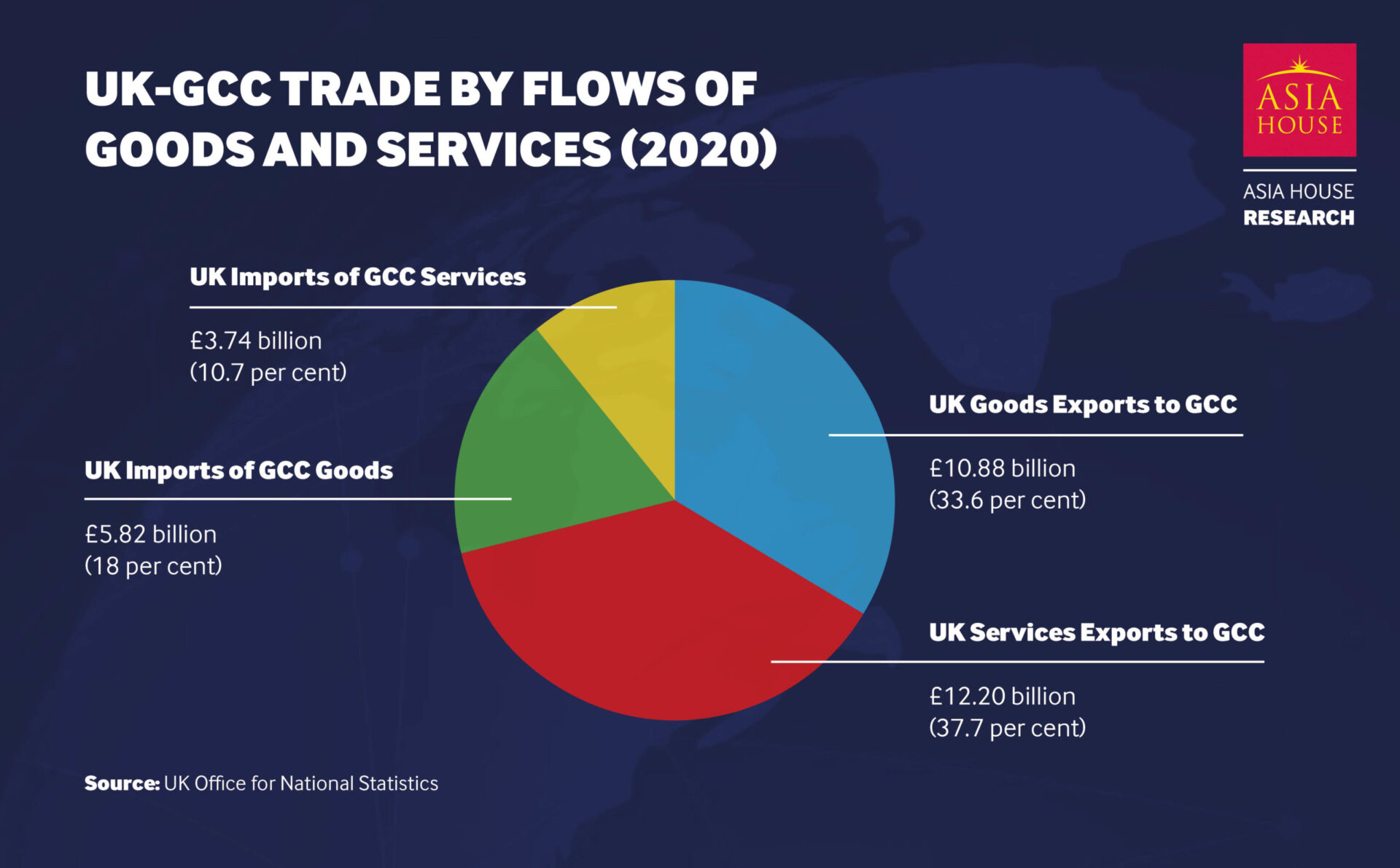

A comprehensive FTA with the GCC – comprising Saudi Arabia, the UAE, Kuwait, Bahrain, Qatar, and Oman – would represent a major milestone in the UK’s post-Brexit global trade agenda. The GCC is the UK’s 10th largest trading partner. Bilateral trade reached £41.4 billion in 2019 but has since fallen to roughly £32.4 billion in 2020 due to the COVID-19 pandemic. The UK also enjoys a notable trade surplus with the GCC worth around £13.8 billion in 2020, creating incentives to broker a deal. (Figure 1).

Figure 1

The GCC has also expressed optimism regarding an FTA with the UK, with Bahrain’s Minister of Industry, Commerce and Tourism, Zayed Al Zayani, recently stating he is hopeful an agreement can be finalised by the end of 2022, or latest by the middle of 2023. The GCC considers the UK as an important economic and political partner. An FTA with the UK could strengthen these ties further. At a time when Gulf states are diversifying their economies, an FTA could also allow them to encourage growth in developing economic sectors.

Gulf economic diversification has led to investment in ports, manufacturing, industry, and the digital economy. This will drive GCC economic and trade growth over the next decade, creating incentives on both sides to broker a deal. Exports from the GCC’s two largest economies, Saudi Arabia and the UAE, in particular are set to rise considerably over the next 10 years. A recent Standard Chartered report projects that Saudi goods exports will rise from US$171 billion to US$354 billion between 2020 and 2030, whereas UAE goods are projected to grow from US$166 billion to US$299 billion over the same period. Approximately 70 per cent of total UK-GCC trade is made up of the UK’s trade with these two economies, highlighting the markets that the UK may privilege during negotiations (Figure 2).

Figure 2

There are benefits on offer for both sides in brokering an FTA and willingness to negotiate. But FTAs vary greatly in terms of the breadth of sectors covered, the scale by which tariffs and non-tariff barriers to trade are removed, and the depth of any sustainability-related provisions enshrined within an FTA’s text. These factors can determine whether an FTA achieves successful outcomes, including trade growth, greater business and investor confidence, and enhanced political and economic ties between parties to an FTA. The UK-GCC trading relationship has particular characteristics that will impact how both sides will approach these issues during negotiations. This section explores what we can expect from UK-GCC FTA negotiations in greater detail.

A greater UK focus on removing non-tariff barriers

Tariffs between the UK and GCC are already relatively low. A recent UK government consultation paper shows the average UK tariff applied on GCC exports, weighted by total export value, stands at just 0.4 per cent. This is largely because tariffs are not applied on oil and gas, which make up the bulk of GCC exports to the UK. By contrast the average GCC tariff applied on UK exports, when weighted by total export value, stands at 4.8 per cent.

While UK negotiators will want to focus on reducing tariffs applied on UK goods to redress this imbalance, there could be a greater focus on removing non-tariff barriers to trade, which currently represents a larger imbalance. Non-tariff barriers relate to regulations, standards, and procedures required of foreign firms to abide by domestic legislation, which can increase trading costs, increase costs of doing business, and reduce trade. The UK government counts 61 non-tariff measures that it applies on GCC members, but counts 4,798 non-tariff measures applied by the GCC on the UK. Attempting to redress this imbalance to improve market access for UK businesses will likely be a key aim for the UK government.

Gulf states will seek concessions in return for greater UK market access

The UK has a large trade surplus with the GCC and faces more barriers to trade with the GCC than the GCC does in its trade with the UK. This gives the UK a greater incentive and room to manoeuvre in terms of improving market access. GCC states may therefore seek concessions beyond the confines of removing barriers to trade in return for granting the UK greater market access. The GCC may seek foreign investment from the UK to support economic diversification, or commitments relating to defence, security, and foreign policy.

The GCC has incentives to negotiate an FTA and is willing to engage with UK negotiators, but the UK government has arguably expended more energy publicly in preparing the ground for negotiations. The UK government has staked a large degree of political capital on crafting an independent trading policy after Brexit through FTAs, which could lead GCC negotiators to believe they are in a good position to extract concessions from the UK.

There are of course non-tariff barriers to trade that the Gulf states could choose to focus on. One concession that the Gulf states will likely seek is on securing visa-free travel to the UK for its citizens. Currently citizens of the UAE, Kuwait, Oman, and Qatar have to pay £30 for an Electronic Visa Waiver (EVW) before travelling to the UK. The EVW allows citizens to visit the UK for up to six months, but citizens must give over 48 hours’ notice before travel, which officials have argued is an impediment on conducting business. By contrast, UK citizens travelling to the majority of GCC countries (UAE, Bahrain, Qatar, and Kuwait), are granted a visa on arrival. Granting Gulf citizens visa free access would remove an important non-tariff barrier to trade for Gulf states.

Both sides have incentives for a broad FTA

Both sides will likely seek a broad FTA that covers a range of sectors. The UK government has indicated its intention to broker a broad FTA, saying it wants to focus on digital trade, services, and green growth, with specific target sectors including food and drink, education, healthcare and life sciences, financial services, and green-tech. GCC economic diversification programmes have increased the Gulf’s incentive to negotiate a broad agreement that includes developing economic sectors that are receiving greater investment and attention from Gulf policymakers.

Recent investments agreed between individual GCC states and the UK, highlight some of the sectors that are the focus of GCC economic diversification and could be focussed on during negotiations. Recent investments include:

The UK is reportedly also close to signing a Sovereign Investment Partnership (SIP) with Saudi Arabia, which once enacted, could indicate sectors that Saudi Arabia will want to see GCC negotiations focus on.

Digital trade chapters are increasingly featured in FTAs, and Gulf negotiators will be receptive to discussions on digital trade during negotiations. The Gulf states have increased investment into their digital economies and efforts to establish favourable regulatory environments to allow the digital economy to flourish. Dubai, for example, introduced a new ‘Virtual Assets Regulatory Authority (VARA)’ in 2022, to regulate the licencing and governance of virtual assets and cryptocurrencies, whereas Saudi Arabia has developed new regulatory sandboxes to encourage growth in its fintech sector. While the Gulf states are investing in digital transformation, jurisdictions also have introduced data localisation provisions, largely to protect residents’ personal data, but which have also been criticised for hampering economic diversification and making data transfers between jurisdictions more difficult.

Sustainability-related provisions have a greater chance of featuring than before

The UK government will attempt to enshrine sustainability-related provisions within a UK-GCC FTA. These provisions have become common-place in FTAs, and address issues relating to the environment, labour rights, and sustainable business practices. While disagreement over sustainability provisions are attributed as one reason why GCC-EU FTA negotiations have stalled, the last few years have seen the Gulf states undertake several social and economic modernising steps that make the inclusion of sustainability-related provisions more likely than before.

2022 has seen the UAE implement revisions to its Labour Law, offering new rights and protections to workers, while Saudi Arabia is expected to soon adopt a new personal status law that is expected to improve women’s rights. Qatar too amended its employment laws in 2020, improving workers’ rights and introduced a minimum wage in March 2021. On the environment, 2021 saw Saudi Arabia, the UAE, and Bahrain, pledge themselves to net-zero carbon emission targets for the first time, increasing the likelihood that environmental provisions will be elevated within any UK-GCC FTA.

While recent economic and social reform does improve scope for the inclusion of greater sustainability-related provisions, such as on labour rights and the environment, than before, it is unlikely that sustainability provisions will reach the same level that the UK has brokered in other FTAs. Language and sustainability-provisions that challenge Gulf models of rule, particularly relating to political freedoms, will be off limits.

While there is currently good will and resolve on both sides to broker an FTA, there are obstacles that could present difficulties for negotiators, particularly on the UK side, which could impact the quality of any UK-GCC FTA.

The GCC has difficulties negotiating FTAs

While the GCC has successfully signed FTAs with Singapore (2008) and the European Free Trade Association[1] (2009), attempts to negotiate FTAs with other countries and trade groups have largely stalled. GCC negotiations with China for example have been ongoing since 2004. The EU has also been unable to iron out an FTA with the region, with discussions faltering in 2010. Similar negotiations with New Zealand, Turkey, and India have also stalled.

There are several reasons why the GCC can struggle to negotiate FTAs. The Gulf states are not homogenous – they are at different stages in their economic diversification journeys, have different strategic and economic priorities, and different regulatory environments, which hamper the GCC’s ability to negotiate from a united standpoint. Economic power is not evenly distributed within the GCC. Gulf states have specific economic sectors that they may wish to prioritise in negotiations. The UAE for example, has shown protectionist tendencies towards its iron and steel industry, increasing tariffs on these commodities to 10 per cent in 2019. Different economic considerations and interests within the GCC could impact their ability to negotiate from a united front and could prompt individual members to block certain provisions.

Indeed, while the GCC was created to facilitate greater economic and political cooperation between member states, at times differences between the Gulf states have undermined this mandate. The 2017-2021 Gulf dispute, which saw Saudi Arabia, the UAE, and Bahrain launch an economic and diplomatic boycott against Qatar, provides clear evidence of the bloc’s propensity for in-fighting. The Gulf states do compete economically and have previously taken steps that undermine GCC economic integration. The UAE, for example, withdrew from preparations to launch a GCC currency and monetary union, just before its launch in 2010. Even the GCC’s most notable achievement, the establishment of a customs union, has occasionally been challenged. The customs union abolishes tariffs on goods produced in the GCC, but in July 2021, Saudi Arabia imposed tariffs ranging up to 15 per cent on products made by any GCC-based company whose workforces relied too heavily on foreign nationals in a bid to stop Saudi firms from being undercut by cheap foreign labour.

Ultimately, the Gulf states do compete with one another economically, and this could impact the GCC’s ability to negotiate from a united front and the UK’s ability to negotiate a comprehensive FTA.

Gulf states may want to prioritise localisation

The Gulf states’ various economic diversification strategies show a propensity for localisation, which may deter the Gulf states from ceding too much ground to UK businesses in terms of improving market access.

The Gulf states’ various economic diversification strategies are aimed at expanding their domestic non-oil industries and encouraging their citizens to move into the private sector. The UAE for example launched ‘Operation 300bn’ in 2021, a decade-long programme to boost the industrial sector’s contributions to UAE GDP to 300 billion dirhams (roughly US$81.67 billion). An important component of Operation 300bn is the UAE’s In-Country Value Program (ICV), which encourages higher public spending on developing new local industries and localising supply chains. Saudi Arabia similarly launched its ‘Made in Saudi’ programme in March 2021, to encourage increased consumption of locally produced goods. ‘Made in Saudi’ is one aspect of the Kingdom’s broader ‘National Industrial Development and Logistics Program’, which was launched in 2019, to invest in domestic industry, manufacturing, and logistics.

The Gulf states have also introduced quotas on firms to hire local staff. The ‘Saudi nationalization scheme’, more commonly referred to as Saudization, for example, offers incentives to firms such as visas, and expedited documentation processing, depending on the number of Saudis they hire. Foreign firms have complained that employment localisation schemes impose costs on them in training or hiring staff to compensate for underskilled local employees.

Finally, localisation provisions are present in rules relating to government procurement in all GCC economies, impacting foreign firms’ ability to compete. Saudi Arabia, Kuwait, and Qatar for example have provisions requiring foreign contractors to subcontract 30 per cent of the tender’s value to local firms, whereas Oman provides a 10 per cent price preference to tenders that use a high degree of Omani goods, services, and labour.

The Gulf states’ tendency towards localisation and efforts to privilege their domestic industries, is embedded within their national economic strategies and could lead to the Gulf states to adopt negotiating positions that prioritise localisation and does not cede too much ground to UK businesses. This could impact the effectiveness of any FTA brokered.

Are GCC states moving towards negotiating FTAs on a bilateral basis?

The above difficulties may account for why some GCC states have opted to negotiate FTAs with other countries bilaterally. Recent weeks have seen the UAE negotiate separate FTAs with both India and Israel. The UAE-India Comprehensive Economic Partnership (CEPA) reportedly cuts duties on 90 per cent of goods traded between them, whereas the UAE-Israel FTA reportedly covers 95 per cent of goods and removes various barriers to trade. The UAE also has an eye on negotiating FTAs with Indonesia and Colombia.

There are benefits for the UK in negotiating a GCC-wide FTA rather than with individual members bilaterally. A GCC-wide FTA would make it easier for UK businesses to operate between jurisdictions within the GCC, and would facilitate broader UK geopolitical aims of encouraging greater economic integration within the Middle East and deepening ties with the GCC. But there is a risk that the difficulties outlined above could lead the UK to negotiate an unsatisfactory FTA which secures limited benefits for UK businesses.

There is willingness on both sides to broker a UK-GCC FTA and clear opportunities to negotiate an agreement that takes an already significant trading partnership to a new level, reduces costs for UK and GCC businesses, further encourages Gulf economic diversification and social reform, and deepens UK-GCC ties. But obstacles do exist, which will need to be at the forefront of negotiators’ minds and will require careful navigation to reduce the risk that negotiations either stall or produce an underwhelming deal that does little to boost trade or improve market access for businesses.

As with previous negotiations, the UK government will publish its response to its recent public consultation and its intended approach to negotiations before formal talks start. These documents will be instructive on the UK’s position, but it is unlikely that there will be a similar public document released by the GCC. The GCC has recently appointed a chief negotiator to lead FTA discussions worldwide, but key decisions and final text will ultimately be approved in Gulf capitals, and it is at this stage that we could see Gulf interests in terms of protecting domestic economic interests play out.

The GCC’s past difficulties negotiating free trade agreements is another clear obstacle to navigate. With some GCC members increasingly negotiating on a bilateral basis, it is plausible that individual members could try to push the UK government to depart from its stated position of negotiating an FTA with the GCC as a bloc, particularly if negotiations begin to falter.

[1] The European Free Trade Association consists of Iceland, Liechtenstein, Norway, and Switzerland.

FIND OUT MORE ABOUT ASIA HOUSE RESEARCH