Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

Driving commercial and political engagement between Asia, the Middle East and Europe

In a new research briefing, Phyllis Papadavid, Head of Research and Advisory at Asia House, identifies a need for Vietnam to generate investment that will boost resilience against emerging risks, despite its success is navigating the COVID-19 crisis.

In a new research briefing, Phyllis Papadavid, Head of Research and Advisory at Asia House, identifies a need for Vietnam to generate investment that will boost resilience against emerging risks, despite its success is navigating the COVID-19 crisis.

Vietnam has been an economic success story and has shown resilience during past crises, including the current COVID-19 pandemic.

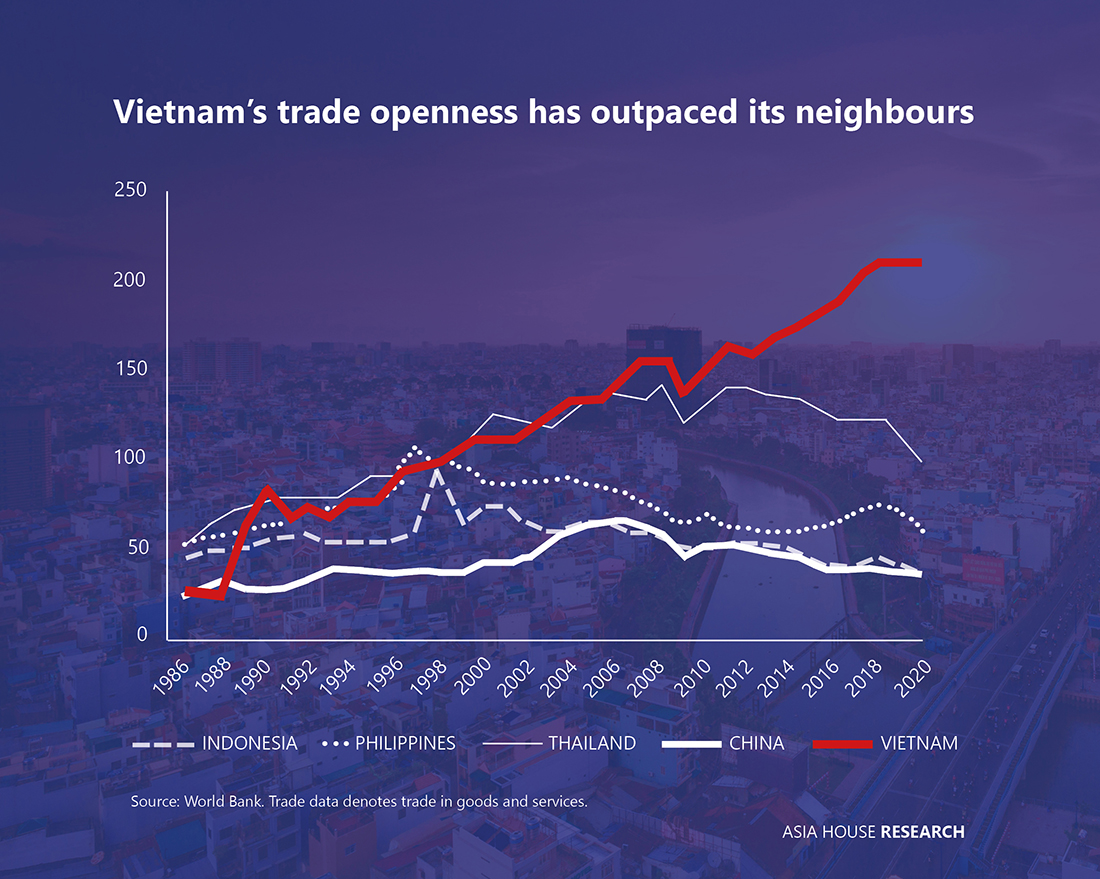

Vietnam is one of Asia’s most open economies to cross-border trade. Trade represented 209 per cent of its GDP in 2020, signifying deep international integration.

With Vietnam facing multiple risks ahead, it is of key importance that it fosters inward investment that enhances resilience against climate change and economic shocks.

Vietnam is one of Asia’s most open economies to cross-border trade, which represented 209 per cent of its GDP in 2020 according to the World Bank – second only to Singapore in the region. Trade liberalisation has played a significant role in Vietnam’s success: it joined the WTO in 2007 and has signed free trade agreements with ASEAN countries, the US and the UK. The Regional Comprehensive Economic Partnership, the world’s largest trade agreement, was signed by Vietnam in 2020.

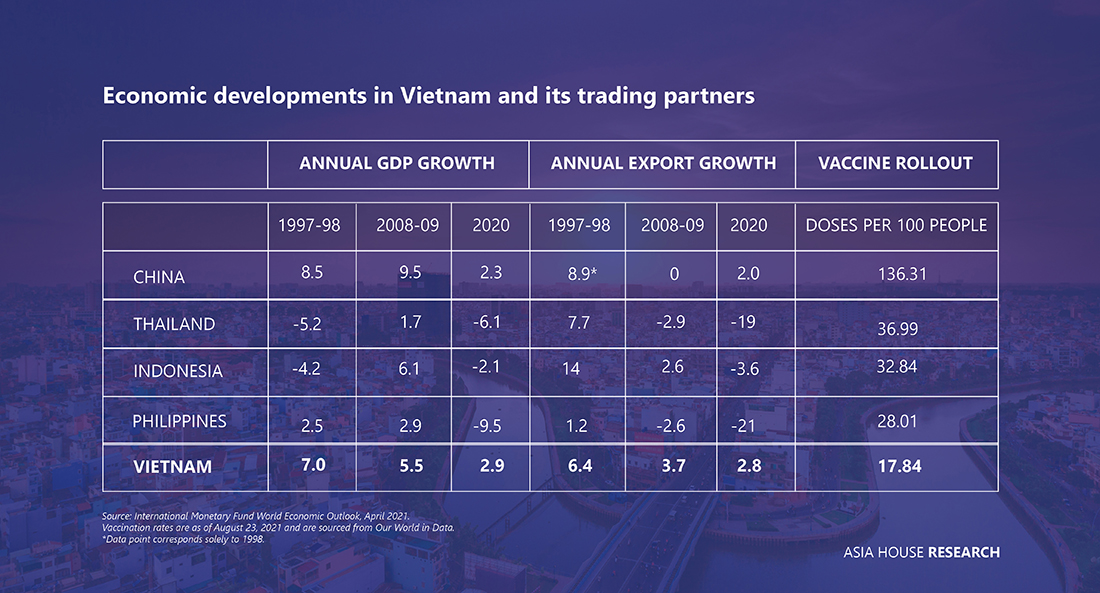

This openness (see Figure 1) has enabled Vietnam to show resilience during the COVID-19 pandemic. Its economy grew in 2020, one of the few to do so. Like many Asian economies, Vietnam is reliant on both the US and China, which are its first and second largest export markets respectively. These relationships are particularly important, given that the current growth downturn is beginning to bear shades of the 1997-98 financial crisis (Figure 2).

Figure 1

Despite a number of production disruptions stemming from supply chain problems related to its COVID-19 factory closures, Vietnam has seen great resilience in its economic growth. However, looking beyond the pandemic, Vietnam is also facing a range of emerging risks that will require a new approach to investment.

Over the past decades, and in the current crisis, Vietnam is largely seen as a success story. And yet, it needs to foster a new kind of investment – the kind which builds resilience against climate risk and the associated uncertainties that it brings. Vietnam is the most exposed country to climate risks in the region, particularly now that its economic resources are constrained by the crisis. Policymakers need to promote the kind of catalytic FDI that was instrumental to the country’s success. Financial investment is also needed to mitigate and insure against climate risk too.

Figure 2

Globally, cross-border investments remain weak amid the COVID-19 crisis. And yet, FDI flows to developing economies in Asia increased by four per cent in 2020, according to UNCTAD. Southeast Asia’s economies did not benefit from this: they experienced a 25 per cent drop in FDI in 2020 – Singapore, Indonesia and Vietnam saw drops. Lockdown measures, repeated waves of COVID-19 infections and supply chain disruption were key factors. FDI is particularly sensitive to the ability to travel, making Vietnam’s tourist sector vulnerable. Looking ahead, risks to Vietnam’s inward investment are likely to stem from:

Vietnam’s low vaccination rate. With only around one per cent of its population fully vaccinated[1], Vietnam’s vaccine rollout has been slow. Taken together with investors’ intermittent risk aversion, stemming in part from the normalisation in US monetary policy, US-China geopolitical tensions, and developments in Afghanistan, this could mean that home bias increases. An increase in home bias would lead to a decline in cross-border investments, particularly in countries or asset classes that are seen to be higher risk. Vietnam would likely be included in this given its low vaccination rate and the associated uncertainty in its investment climate from repeated COVID-19 waves of infection.

Factory closures and supply-chain disruptions are impacting Vietnam’s export-led industrialisation efforts. Lockdowns in response to periodic waves of COVID-19 infections have led to factory shutdowns, which have in turn disrupted global supply chains. Major footwear companies, such as Foot Locker and Adidas, have cited challenges. Ho Chi Minh City, Vietnam’s largest city, has been impacted particularly strongly; it imposed strict social-distancing measures including rules on worker transport and housing, and the deployment of staff on factory floors. Vietnam’s Textile and Apparel Association has voiced strong concern over the impact of COVID-19 on the country’s outlook. The risk of further supply chain disruption to Vietnam’s export outlook is particularly high given the country’s low vaccination rate.

Vietnam is particularly exposed to climate risks. Flooding represents the largest risk by economic impact in Vietnam, according to the Asian Development Bank. It estimates that the population affected annually by flooding is estimated at 930,000 with an annual impact on GDP of US$2.6 billion. An estimated 2.4 per cent of Vietnam’s GDP is at risk from permanent inundation in the Red River Delta region, according to the World Bank. Approximately 10 per cent of the Hanoi region’s GDP is vulnerable to permanent inundation due to sea level rise, and more than 40 per cent is vulnerable to periodic storm surge damage. Moreover, sea-level rise would exacerbate damage caused by cyclone-induced storm surges.

Of the three risks, the third poses the most significant challenge in the longer term. Investments, and particularly those that build resilience to climate change, are of paramount importance. Vietnam should build on past success towards the sustainable development goals (SDG). It typically ranks in the top quarter of SDG performance across the Southeast Asian region for several SDG sub-indicators. Power generation, transmission, and distribution capacity have been scaled up to meet rapidly rising electricity demand with Vietnam’s per capita electricity consumption more than tripling over the past decades. Access to paved roads is high, and rural household electrification increased from below 50 per cent in 1990 to 99 per cent in 2016.

FDI has been pivotal to Vietnam’s economic growth. It has complemented its infrastructure development. Over the past decade, government capital spending has averaged almost eight per cent of GDP annually, according to the International Monetary Fund. In addition, state-owned enterprises have invested about five per cent of GDP annually. National and provincial government is working to protect the coastline, primarily through hard infrastructure and mangrove restoration. Vietnam’s Green Growth Strategy aims to transition the country into a low carbon economy, enrich natural capital and achieve sustainable development through innovative digital technology.

More should be done to promote and prioritise the following types of investment:

FDI in agricultural technology (AgTech). Biotechnology, automation, and information technology are fundamental for Vietnam’s green economy. Its three most prominent zones in this sector are Hau Giang, Phu Yen, and Bac Lieu provinces. Foreign agricultural firms such as Germany’s Bayer Global and Thailand’s Charoen Pokphand have also been important. Developments in Green Bond certification will also augur well for raising finance for enterprises in the AgTech sector.

FDI that promotes the spatial re-patterning of the economy through creating new economic clusters in non-coastal areas, and generating employment opportunities, will help build resilience. FDI has contributed to poverty reduction both directly through boosting growth, and indirectly through Vietnam’s human capital development. The spatial re-patterning that is needed in Vietnam could necessitate, in part, an investment diversification away from the coastal tourism industry.

Disaster risk financing and insurance is key to managing the costs of Vietnam’s natural disasters. Determining adequate levels of post-disaster financing and the government’s contingent liabilities linked to natural disasters is an important first step. Globally, there is evidence to suggest that the financing gap is significant for flood losses. The onus is on Vietnam to institute investment facilities, including blended finance, that include the public and private sectors, to improve disaster preparedness.

While Vietnam’s policymakers have made significant progress in achieving sustained growth, a new policy push is needed to meet the challenges ahead. Much of Vietnam’s success has stemmed from it leveraging its international integration. It now needs to further focus its efforts on fostering investments to build resilience against climate and economic shocks. Implementing a comprehensive risk financing strategy will also be crucial at a time when financial markets could continue to show risk aversion. Vietnam’s past efforts to implement reforms have been successful and augur well for the challenges ahead.

[1] Data as of 23 August 2021.

HE Nguyen Hoang Long, Vietnam’s Ambassador to the UK, will brief Asia House Corporate Members on Vietnam’s economy on Wednesday 1 September. Find out more.

JOIN OUR MAILING LIST to receive Asia House insights, analysis and research direct to your inbox.